Elina Ward

Member

- Messages

- 86

- Likes

- 1

Thursday 23 April 2026

Brent Crude Extends Rally Above $106 as Middle East Risk Premium Builds

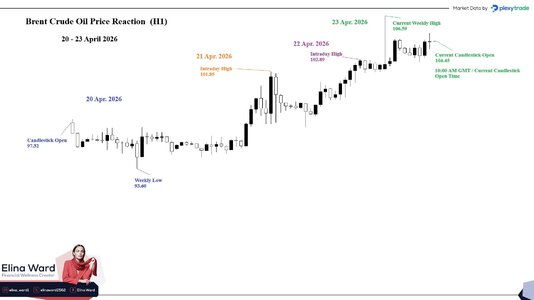

Brent crude oil advanced sharply through the week of April 20–23, rebounding from early losses to multi-day highs as geopolitical tensions in the Middle East drove a sustained repricing of supply risk.The week opened near $97.52 on April 20, with prices initially softening to a weekly low of $93.60 amid cautious sentiment and the absence of immediate disruption signals. However, the tone shifted decisively on April 21, when Brent reversed higher and broke through the $100 threshold, reaching an intraday high of $101.85.

The move marked a clear inflection point in market positioning. Rather than reacting to a single headline, oil markets began gradually pricing in rising uncertainty around Gulf shipping routes and ongoing U.S.–Iran tensions. This resulted in a steady, structured advance rather than a sharp, news-driven spike.

Momentum carried into April 22, with Brent extending gains to $102.89, before accelerating further into April 23. Prices climbed to a weekly high of $106.59, reflecting a +12.99 move (+13.88%) from the weekly low. The contract was last seen with a current candlestick open around $104.45 during the European session.

Technically, the rally remained well-supported, with a consistent sequence of higher highs and higher lows reinforcing bullish structure. The absence of aggressive pullbacks suggested the move was driven by sustained institutional positioning rather than short-term speculative flows.

The broader backdrop remained anchored in geopolitical developments, including unresolved negotiations between the United States and Iran, as well as persistent concerns around potential disruptions to oil flows in the Gulf. While no major oil company announcements materially shifted supply expectations during the period, the geopolitical risk premium continued to build.

Price Action Summary (20–23 April 2026)

| Metric | Value |

|---|---|

| Weekly Open | 97.52 |

| Period High | 106.59 |

| Period Low | 93.60 |

| Latest Price (Apr 23 Open) | 104.45 |

| Total Move (Low → High) | +12.99 (+13.88%) |

| Net Move (Open → Latest) | +6.93 (+7.10%) |

| Total Range | 12.99 (~1,299 ticks) |

Summary

Oil markets once again demonstrated how strongly geopolitical developments influence price action. From a weekly low of $93.60 to a high of $106.59, Brent crude recorded a +12.99 move, equivalent to +13.88%, as markets steadily priced in rising uncertainty rather than reacting to a single event.Geopolitics plays a critical role in oil because a large portion of global supply flows through politically sensitive regions, particularly the Middle East. Any escalation, disruption risk, or breakdown in diplomatic progress directly affects expectations around supply availability, prompting markets to reprice risk in real time.

In this case, the absence of a clear resolution, combined with ongoing tensions and shipping concerns, led to a sustained build-up of risk premium. The result was a structured upward move, highlighting how oil markets are driven not just by actual disruptions, but by the evolving probability of them.

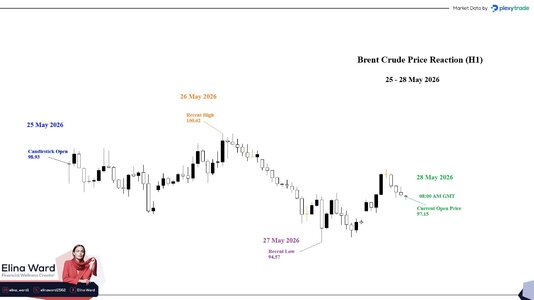

The chart below represents Brent crude oil price action on an H1 timeframe, covering the period from April 20 to the current movement on April 23, 2026.