Belligerent_Drunk

Junior member

- Messages

- 38

- Likes

- 4

Hi all,

I am opening this thread because I want to build up a constructive discussion of how people evaluate their trading strategies, wether they are manual or automated strategies.

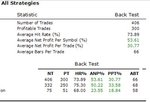

The reason I bring this up, is that I recently started toying with some automated strategies and want to figure out how I can analyze the results coming out of a backtest better. I am building a spreadsheet for this purpose and I'm looking for improvements. Just curious how you guys tackle this problem.

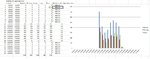

I've attached snaps of the spreadsheet. It's WIP, since I need to add a whole list of things (including changing winners to green and losers to red in the chart hehe).

I am opening this thread because I want to build up a constructive discussion of how people evaluate their trading strategies, wether they are manual or automated strategies.

The reason I bring this up, is that I recently started toying with some automated strategies and want to figure out how I can analyze the results coming out of a backtest better. I am building a spreadsheet for this purpose and I'm looking for improvements. Just curious how you guys tackle this problem.

I've attached snaps of the spreadsheet. It's WIP, since I need to add a whole list of things (including changing winners to green and losers to red in the chart hehe).