Agree with DT & Jack here.

Stat arb is quite often HFT turf so impractical for most.

Longer term trades although not directional still carry risk,

especially with stock spreads.

If the correlation is just sector related and the stock you are short

continues and breaks the sector correlation altogether for instance.

E-mini - Wikipedia, the free encyclopedia

http://www.futuresindustry.org/downloads/Audio/Companion/Three-812.pdf

Salient points of above PDF highlighted below:

Just my view, but I think if you are going to try longer term spread trading,

I would stick to U.S. indices.

Different ES contracts or ES against synthetic ES (made up of YM, NQ and ER2)

Or find another sythetic combo:

More examples:

5 Year US Treasury Future – 10 Year US

Treasury Future.

2 Year US Treasury Future – 5 Year US

Treasury Future as a Package against the

10Year US Treasury Future – 30 Year US

Treasury Future Package.

Other pairs could be:

Dax – EuroStoxx

CAC –FTSE

Not so keen on the above Euro indices, as I personally think any correlation is just sentiment based.

Sector and industry weighting are potential correlation breaks.

In a nutshell its free money for the HFT stat arb outfits.

For anyone else there are still risks.

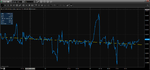

Examples from above pdf:

ES up 5.0 points, YM down 50 on CAT

earnings worries.

GE – HON Take over Arbitrage Spread was

trading at 0.60 and blew out to over 12.00

when the Deal fell through.

LTCM Yield Convergence trade blew up

when Russia Defaulted.

2 Year TED Spread went from 35 bps to 75

bps when plane hit WTC.

It can be a good method, even excellent with the right tools and resources.

It can also be an over complex, over leveraged disaster waiting to happen.

Don't forget, the man with the large cojones was spread trading...

😆

I would say his name but he might come back

😱