Hi

Im trying to understand the option neutral strategy straddle.

Investopedia defines straddle in the following manner:

"A straddle is an options strategy with which the investor holds a position in both a call and put with the same strike price and expiration date. This allows the investor to make a profit regardless of whether the price of the security goes up or down, assuming the stock price changes dramatically. "

My understanding is that is a neutral strategy, it does not matter if the price moves up or down, so far so good.

Everyone recommends to buy at the money put and calls for the strategy.

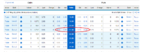

When you look at a option chain for a stock (please look attached file) either the put or the call has to be out of the money while the other is at the money.

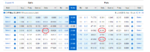

Another thing is that you are supposed to buy the same strike and the same expiration. But when you purchased the same strike for the put and the call then you realized that the option has not the same delta (please see attached file "Chain Greeks"), so the options do not move the same.

The stock symbol that I use for the example is "CNP" and when I took the picture the price was 21,68, if you calculate the breakeven price for the call and the put using the same strike price in this case 21 and the same expiration in this case 10 days you realize that for the call the price only needs to move 1,2% upwards and for the put it needs to move 4,52% downwards to breakeven.

The strategy is suppose to be neutral and is suppose to make money if it moves up or down a lot, but what I see and I have check in many stocks and it happens the same is that the trade is skewed in one direction since the move upwards to be profitable is considerable smaller than the move that needs to make downwards, so is not very neutral.

By my understanding to be neutral it will need to have the same delta so the price of the options move the same which in this case is not, and the possibility of making money long or short should be the same which in this case is clearly not since for the call you only need a move of 1,2% to breaeven but for the put you need a much bigger move of 4,52% to breakeven.

Please could someone explained to me or tell me what Im getting wrong, I would really appreciated

Thanks

Im trying to understand the option neutral strategy straddle.

Investopedia defines straddle in the following manner:

"A straddle is an options strategy with which the investor holds a position in both a call and put with the same strike price and expiration date. This allows the investor to make a profit regardless of whether the price of the security goes up or down, assuming the stock price changes dramatically. "

My understanding is that is a neutral strategy, it does not matter if the price moves up or down, so far so good.

Everyone recommends to buy at the money put and calls for the strategy.

When you look at a option chain for a stock (please look attached file) either the put or the call has to be out of the money while the other is at the money.

Another thing is that you are supposed to buy the same strike and the same expiration. But when you purchased the same strike for the put and the call then you realized that the option has not the same delta (please see attached file "Chain Greeks"), so the options do not move the same.

The stock symbol that I use for the example is "CNP" and when I took the picture the price was 21,68, if you calculate the breakeven price for the call and the put using the same strike price in this case 21 and the same expiration in this case 10 days you realize that for the call the price only needs to move 1,2% upwards and for the put it needs to move 4,52% downwards to breakeven.

The strategy is suppose to be neutral and is suppose to make money if it moves up or down a lot, but what I see and I have check in many stocks and it happens the same is that the trade is skewed in one direction since the move upwards to be profitable is considerable smaller than the move that needs to make downwards, so is not very neutral.

By my understanding to be neutral it will need to have the same delta so the price of the options move the same which in this case is not, and the possibility of making money long or short should be the same which in this case is clearly not since for the call you only need a move of 1,2% to breaeven but for the put you need a much bigger move of 4,52% to breakeven.

Please could someone explained to me or tell me what Im getting wrong, I would really appreciated

Thanks