Risk management isn't just about having your 'stop-loss' in place. So what else is it about?

Any trader who knows his salt will tell you that Risk Management is the single most important aspect in trading, regardless of style or technical strategy. Yet, most traders are really not able to define what "Risk Management" really is. Let's pause for a moment, and think: can we define, in one brief sentence, what Risk Management is? "Loss control" would probably be the best broad definition, but to me this is a little more precise: In the business of trading the financial markets, Risk Management is the constant modulation of Risk Exposure to a constantly changing market. What is this exactly?

Most participants will relegate their entire Risk Management strategy to setting and adhering to "stop losses." But this falls far short of what Risk Management really is. To relegate the entire Risk Management strategy down to simple stop losses would be equivalent to saying "I am safe in my car because I have brakes." Needless to say, the "brakes" are only part of an entire system of managing risk in a constantly moving environment such as street traffic. In this sense, the markets are the same as the streets. There are far more actions we can take to minimize risk besides the brakes: there is steering, controlling the throttle, the path you take, "your trip preparation," mapping your route, the times you drive, the amount of driving you do, not driving while "under the influence," there are so many factors that affect risk levels, that we cannot possibly reduce the entire risk control strategy down to "brakes," or in the case of trading, "stop losses."

So what do we mean by "modulation of Risk Exposure?" How we make and lose money is the end result of our interaction with the market. If we do not interact, we neither win nor lose. If we interact too much, we assume higher levels of risk that may be "more than we can handle." Risk Management is the constant "adjustment" of our Risk Exposure based upon two primary factors: market conditions and, more importantly, our very own performance.

How do we modulate or "adjust" our Risk Exposure? There are 3 primary ways of modulating exposure:

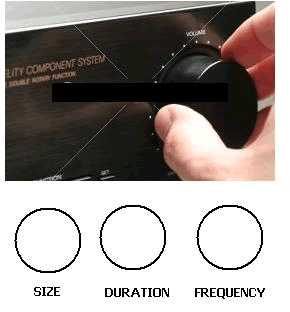

In modulating Risk Exposure, imagine that we have a dial, much like the volume dial on a common stereo. When we want to increase exposure, we "raise" the "volume dial" and vice versa when we want to decrease exposure or move to "off:"

But we really have 3 "volume dials." One to adjust Size, a second one for Duration and a third one for Frequency. As we increase one, we compensate by lowering another.

The biggest single error most traders commit is to take one or more of the dials and twist it to the maximum. In essence, they "blow-out the speakers." In our analogy, the "speakers" would be the trading account!

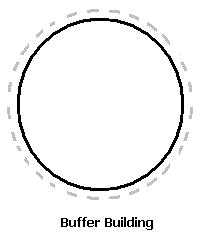

A critical part of Risk Management, particularly for beginners, is to only increase the Risk Exposure whenever we have built what we call "Buffer Zones:"

It is surprising that most traders do not recognize the idea of Buffer Building. In the figure above, the inner black circle represents our trading capital. Our job as traders is to initially build a small buffer around that capital, perhaps only a few % of the account value. This is represented by the dotted gray line, and will serve as the trader's primary goal - to build the Buffer around the account with limited exposure. Once the buffer is achieved, then and only then can he "increase" the volume dial to a higher rate of exposure. He then will set a NEW Buffer zone to build around his capital in order to protect him from future increases in risk exposure, but only increasing exposure once the buffer is built. This process continues perpetually for the trader's life time.

A trader who is correctly managing his risks therefore exists only in one of two primary states: BUFFER BUILDING and CAPITAL PRESERVATION. If he is not building Buffers, he is protecting capital. The state of CAPITAL PRESERVATION is the process of trading at absolute minimum risk exposure until the Buffer is regained.

This method provides the trader a specific focus on exactly what he needs to do, and setting goals that are well-defined, achievable and incremental in nature. Having the correct focus makes "discipline" easier to carry-out. Build your buffers and modulate your risk: this is the simple process and path you need to take to grow your account. Stop-losses are a critical part of this process, but it is merely a piece of a larger, more important process.

Any trader who knows his salt will tell you that Risk Management is the single most important aspect in trading, regardless of style or technical strategy. Yet, most traders are really not able to define what "Risk Management" really is. Let's pause for a moment, and think: can we define, in one brief sentence, what Risk Management is? "Loss control" would probably be the best broad definition, but to me this is a little more precise: In the business of trading the financial markets, Risk Management is the constant modulation of Risk Exposure to a constantly changing market. What is this exactly?

Most participants will relegate their entire Risk Management strategy to setting and adhering to "stop losses." But this falls far short of what Risk Management really is. To relegate the entire Risk Management strategy down to simple stop losses would be equivalent to saying "I am safe in my car because I have brakes." Needless to say, the "brakes" are only part of an entire system of managing risk in a constantly moving environment such as street traffic. In this sense, the markets are the same as the streets. There are far more actions we can take to minimize risk besides the brakes: there is steering, controlling the throttle, the path you take, "your trip preparation," mapping your route, the times you drive, the amount of driving you do, not driving while "under the influence," there are so many factors that affect risk levels, that we cannot possibly reduce the entire risk control strategy down to "brakes," or in the case of trading, "stop losses."

So what do we mean by "modulation of Risk Exposure?" How we make and lose money is the end result of our interaction with the market. If we do not interact, we neither win nor lose. If we interact too much, we assume higher levels of risk that may be "more than we can handle." Risk Management is the constant "adjustment" of our Risk Exposure based upon two primary factors: market conditions and, more importantly, our very own performance.

How do we modulate or "adjust" our Risk Exposure? There are 3 primary ways of modulating exposure:

- SIZE: How large or small our positions are, based on our account values. The more we expose our account, the "larger" the exposure.

- FREQUENCY: How often we are in-and-out of the market. The more frequently we trade, the more we are exposed to the markets' motions over time, the more risk we assume. Also, commission costs become a factor that significantly affects risk levels as we increase frequency.

- DURATION: The longer we are in each trade, the more opportunity the market has to travel, the higher our risks will be.

In modulating Risk Exposure, imagine that we have a dial, much like the volume dial on a common stereo. When we want to increase exposure, we "raise" the "volume dial" and vice versa when we want to decrease exposure or move to "off:"

But we really have 3 "volume dials." One to adjust Size, a second one for Duration and a third one for Frequency. As we increase one, we compensate by lowering another.

The biggest single error most traders commit is to take one or more of the dials and twist it to the maximum. In essence, they "blow-out the speakers." In our analogy, the "speakers" would be the trading account!

A critical part of Risk Management, particularly for beginners, is to only increase the Risk Exposure whenever we have built what we call "Buffer Zones:"

It is surprising that most traders do not recognize the idea of Buffer Building. In the figure above, the inner black circle represents our trading capital. Our job as traders is to initially build a small buffer around that capital, perhaps only a few % of the account value. This is represented by the dotted gray line, and will serve as the trader's primary goal - to build the Buffer around the account with limited exposure. Once the buffer is achieved, then and only then can he "increase" the volume dial to a higher rate of exposure. He then will set a NEW Buffer zone to build around his capital in order to protect him from future increases in risk exposure, but only increasing exposure once the buffer is built. This process continues perpetually for the trader's life time.

A trader who is correctly managing his risks therefore exists only in one of two primary states: BUFFER BUILDING and CAPITAL PRESERVATION. If he is not building Buffers, he is protecting capital. The state of CAPITAL PRESERVATION is the process of trading at absolute minimum risk exposure until the Buffer is regained.

This method provides the trader a specific focus on exactly what he needs to do, and setting goals that are well-defined, achievable and incremental in nature. Having the correct focus makes "discipline" easier to carry-out. Build your buffers and modulate your risk: this is the simple process and path you need to take to grow your account. Stop-losses are a critical part of this process, but it is merely a piece of a larger, more important process.

Last edited by a moderator: