Hi Krzysiaczek99,

I found your tests very interesting. Clearly noise affects the performance as Noxa themselves seem to admit. Nevetheless CSSA remain profitable as the noise change and this is not a mean achievement unless it were due to pure chance !

Your consideration that PF should "not fall at least in case when we move to lower noise conditions. " is thought provoking and I would invite Noxa to comment on that specific point.

The bottomline is perhaps that one cannot expect perfect performance and therefore it would be of value to all of us to be able to assess the limits of CSSA in comparison with other available indicators. Have you any views about this ?

Thanks.

alby1714

I found your tests very interesting. Clearly noise affects the performance as Noxa themselves seem to admit. Nevetheless CSSA remain profitable as the noise change and this is not a mean achievement unless it were due to pure chance !

Your consideration that PF should "not fall at least in case when we move to lower noise conditions. " is thought provoking and I would invite Noxa to comment on that specific point.

The bottomline is perhaps that one cannot expect perfect performance and therefore it would be of value to all of us to be able to assess the limits of CSSA in comparison with other available indicators. Have you any views about this ?

Thanks.

alby1714

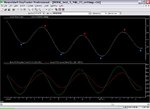

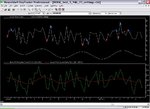

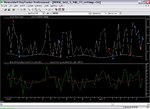

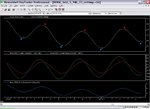

First I agree MACD PF rise is coincidental and not important here, it's simple EMA strategy and it does not distinguish between noisy and not nosy markets.

Regarding CSSA. In my opinion it simple learns cycle and noise, this is the reason that i was calling this 'curve fitting' to noise. So when noise level changes it starts to under

perform because is not adapted to level of a new noise. So it doesnt extract cycle correctly, if it would extract correctly (clean signal which was the same in GOLD5 and -9db) PF would not fall at least in case when we move to lower noise conditions. The settings which were extracting cycle correctly in one case should extract cycle in another because it is the same cycle.

Than it is very risky business to use it if it is not able to filter out noise well. Does it has filtering mechanism build in ?? Which filters if any ?? On the other hand GroupStart and GroupDepth settings should filter noise i guess. So why PF falls ??

Krzysztof