HFM.

Senior member

- Messages

- 2,282

- Likes

- 0

Date 30th June 2023.

Market Update – June 30 – Eyes on PCE.

US ECONOMY

The surprisingly strong GDP revisions and the drop in jobless claims raised fears the FOMC will have to tighten rates further and boosted Treasury yields higher. The bear flattening trade boosted rates to the highest levels since March, the last time the markets fretted over aggressive Fed action. Fed funds futures priced in another hike in the coming months. Asian markets traded mixed, European and US futures are mostly higher as markets wait for the US PCE numbers after yesterday’s strong round of data that lifted Treasury yields.

Biggest Mover @ (06:30 GMT) BCHUSD (+19%) rallied to 322.93 high. Fast MAs flattened, MACD lines are still positively configured with RSI at 80.85 and Stochastic at 57 and falling.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – June 30 – Eyes on PCE.

US ECONOMY

The surprisingly strong GDP revisions and the drop in jobless claims raised fears the FOMC will have to tighten rates further and boosted Treasury yields higher. The bear flattening trade boosted rates to the highest levels since March, the last time the markets fretted over aggressive Fed action. Fed funds futures priced in another hike in the coming months. Asian markets traded mixed, European and US futures are mostly higher as markets wait for the US PCE numbers after yesterday’s strong round of data that lifted Treasury yields.

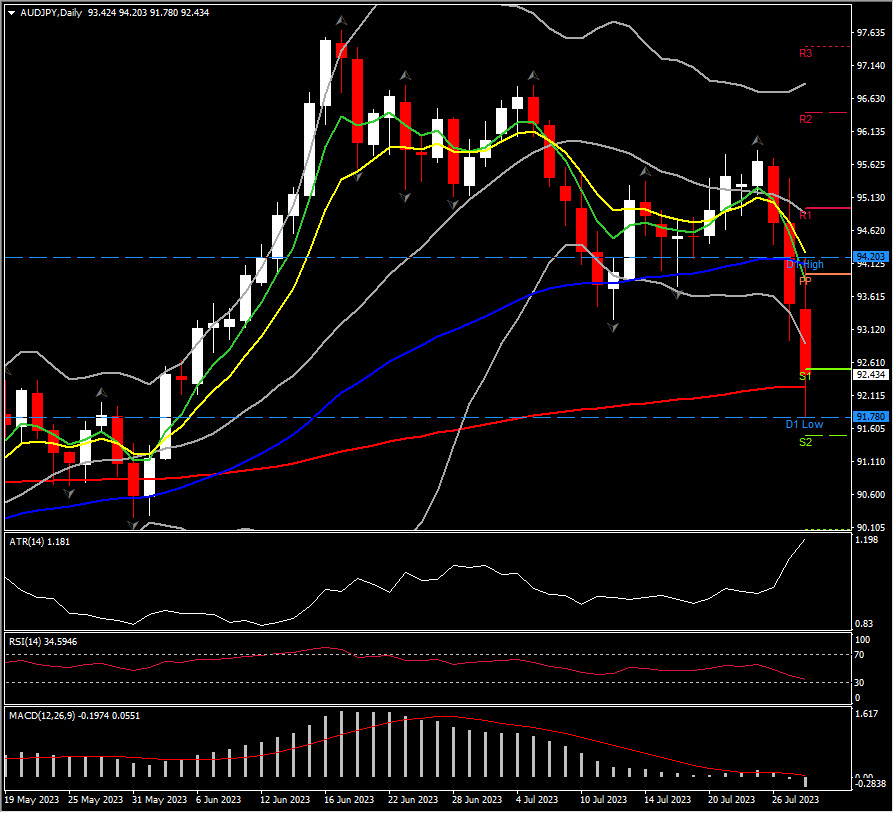

- FX – The USDIndex popped to 103.437 on the more hawkish Fed outlook, but faded to 103.32. USDJPY breached 145. GBP and EUR remained under pressure.

- Stocks – The US30 and US500 are up 0.80% and 0.45%, respectively, supported by financials after the banks passed their stress tests. The US100 was unchanged.

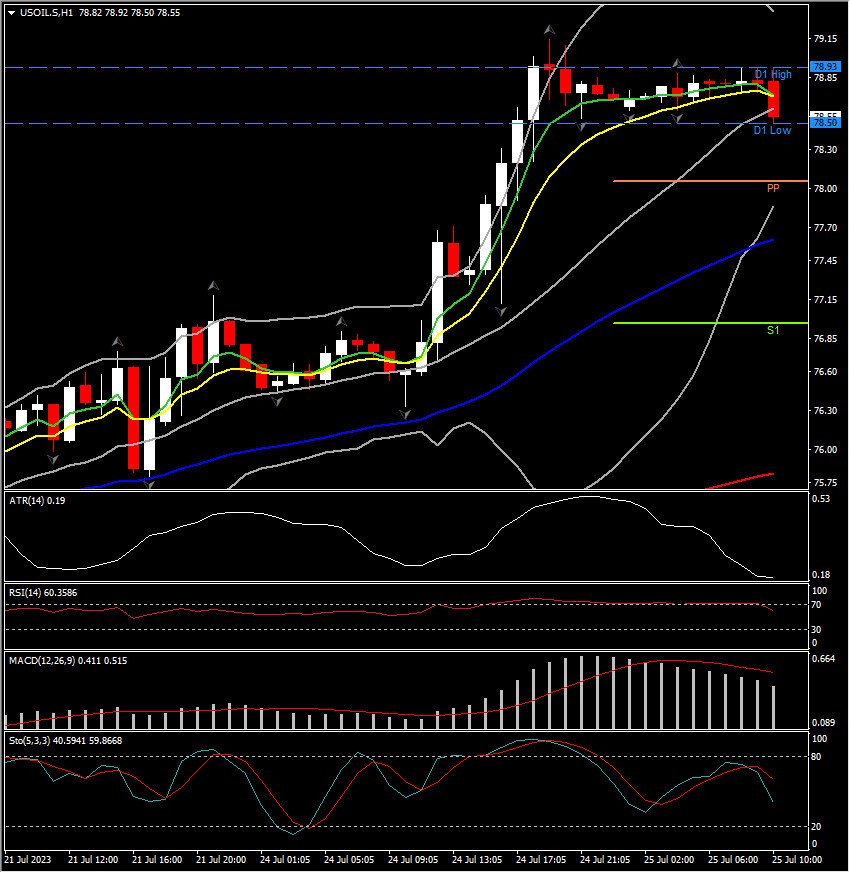

- Commodities – USOil keeps retesting $70. US and European central banks remain hawkish and signal a higher-for-longer stance. China hasn’t delivered the hoped for aggressive stimulus program, but for Russia jitters have eased and a drop in US crude inventories helped to underpin prices today. EIA data showed that US crude inventories dropped by 9.6 million barrels last week – the largest drawdown in more than a month.

- Gold – broke below $1900 level yesterday but quickly returned higher to $1906.

Biggest Mover @ (06:30 GMT) BCHUSD (+19%) rallied to 322.93 high. Fast MAs flattened, MACD lines are still positively configured with RSI at 80.85 and Stochastic at 57 and falling.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.