HFM.

Senior member

- Messages

- 2,282

- Likes

- 0

Date 31st July 2023.

Market Update – July 31 – Another month of gains for stocks comes to an end.

Last Friday, the headline PCE figure for June came in at 3%, the lowest annual increase since March 2021 and just one percentage point over the Fed’s target of 2% inflation; Core set at 4.1. US indices cheered the data and are set for another strong month of gains, the fifth in a row for the US500 that is up 3% in July compared to Nasdaq which has increased 3.8%. Industrial production y/y fell in Japan as did retail sales on a monthly basis; in China, manufacturing PMI is still in contraction (49.3), while the services component is deteriorating (51.5 from 53.2). China just issued measures to recover and expand consumption as per a State Council Document just released. JPY keeps collapsing despite the ”adjustment” on the 10y policy: last Friday a mysterious buyer stepped in at 0.57%, today the BOJ officially announced unscheduled bond buying at 0.60%. This week we have the BOE and RBA (the latter tomorrow morning, expected to raise by 25 bps to 4.35% despite the latest inflation data), US NFP data and the earnings season continues with AAPL and AMZN reporting on Thursday.

Today: Germany retail sales, GDP from Italy, Spain and Europe, European HICP, US Chicago Purchasing Managers’ Index.

Biggest Mover: (@6:30 GMT) Coffee (-2.11%) trading at $158.60 heading south towards the recent $154.50 bottom area. RSI at 41.46 and downward sloped, MACD negative, 50d – 200d MAs downward sloped (and have recently crossed).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 31 – Another month of gains for stocks comes to an end.

Last Friday, the headline PCE figure for June came in at 3%, the lowest annual increase since March 2021 and just one percentage point over the Fed’s target of 2% inflation; Core set at 4.1. US indices cheered the data and are set for another strong month of gains, the fifth in a row for the US500 that is up 3% in July compared to Nasdaq which has increased 3.8%. Industrial production y/y fell in Japan as did retail sales on a monthly basis; in China, manufacturing PMI is still in contraction (49.3), while the services component is deteriorating (51.5 from 53.2). China just issued measures to recover and expand consumption as per a State Council Document just released. JPY keeps collapsing despite the ”adjustment” on the 10y policy: last Friday a mysterious buyer stepped in at 0.57%, today the BOJ officially announced unscheduled bond buying at 0.60%. This week we have the BOE and RBA (the latter tomorrow morning, expected to raise by 25 bps to 4.35% despite the latest inflation data), US NFP data and the earnings season continues with AAPL and AMZN reporting on Thursday.

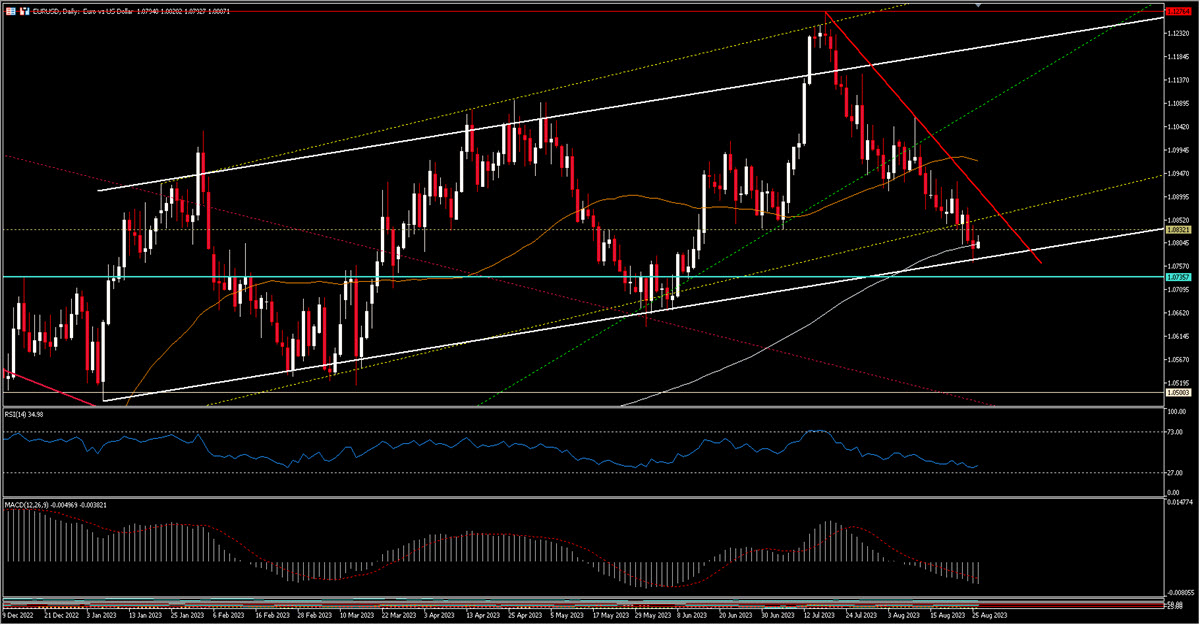

- FX – USDIndex is up 0.2% to 101.61 boosted by a weak Yen (USDJPY -0.46% at 141.81). EURUSD sits just above 1.10, Cable hovers around 1.285, AUDUSD is bid before the RBA tomorrow (+0.51% at 0.6681).

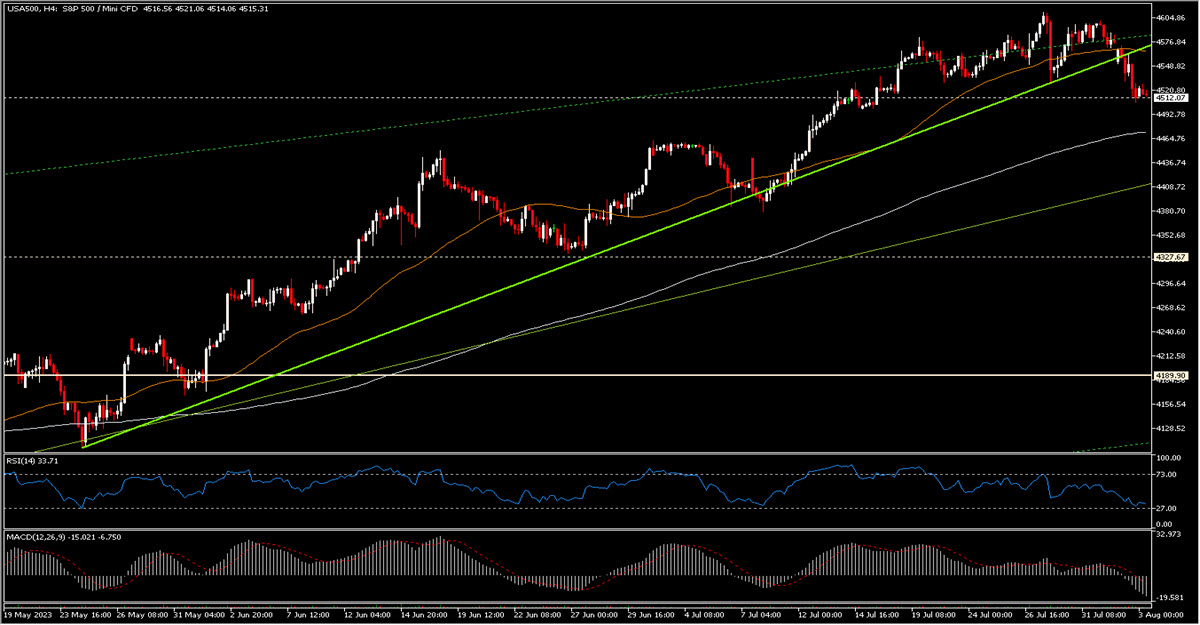

- Stocks – US futures are slightly in red: US500 -0.13%, US30 -0.07%, US100 -0.17%. A similar picture in Europe where GER40 futures are -0.14%. GOOGL increased 10% last week and the US market is set for another month of (broad) gains.

- Commodities – USOil -0.5% now at $80.25, UKOil hit $85 and is now at $84.51.

- Gold – down -0.23% to $1954.91, XAG – 0.40% at $24.24.

USDJPY, 30 mins

Today: Germany retail sales, GDP from Italy, Spain and Europe, European HICP, US Chicago Purchasing Managers’ Index.

Biggest Mover: (@6:30 GMT) Coffee (-2.11%) trading at $158.60 heading south towards the recent $154.50 bottom area. RSI at 41.46 and downward sloped, MACD negative, 50d – 200d MAs downward sloped (and have recently crossed).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.