HFM.

Senior member

- Messages

- 2,282

- Likes

- 0

Date : 14th November 2022.

Market Update – November 14.

Biggest FX Mover @ (06:30 GMT) BTCUSD (+1.12%) rebounded to 16890 but struggling to break 50-hour SMA. MAs aligning higher, MACD lines still negative, RSI 53 & flat indicating that this might be a limited bounce. H1 ATR 313.46, Daily ATR 1334.606.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – November 14.

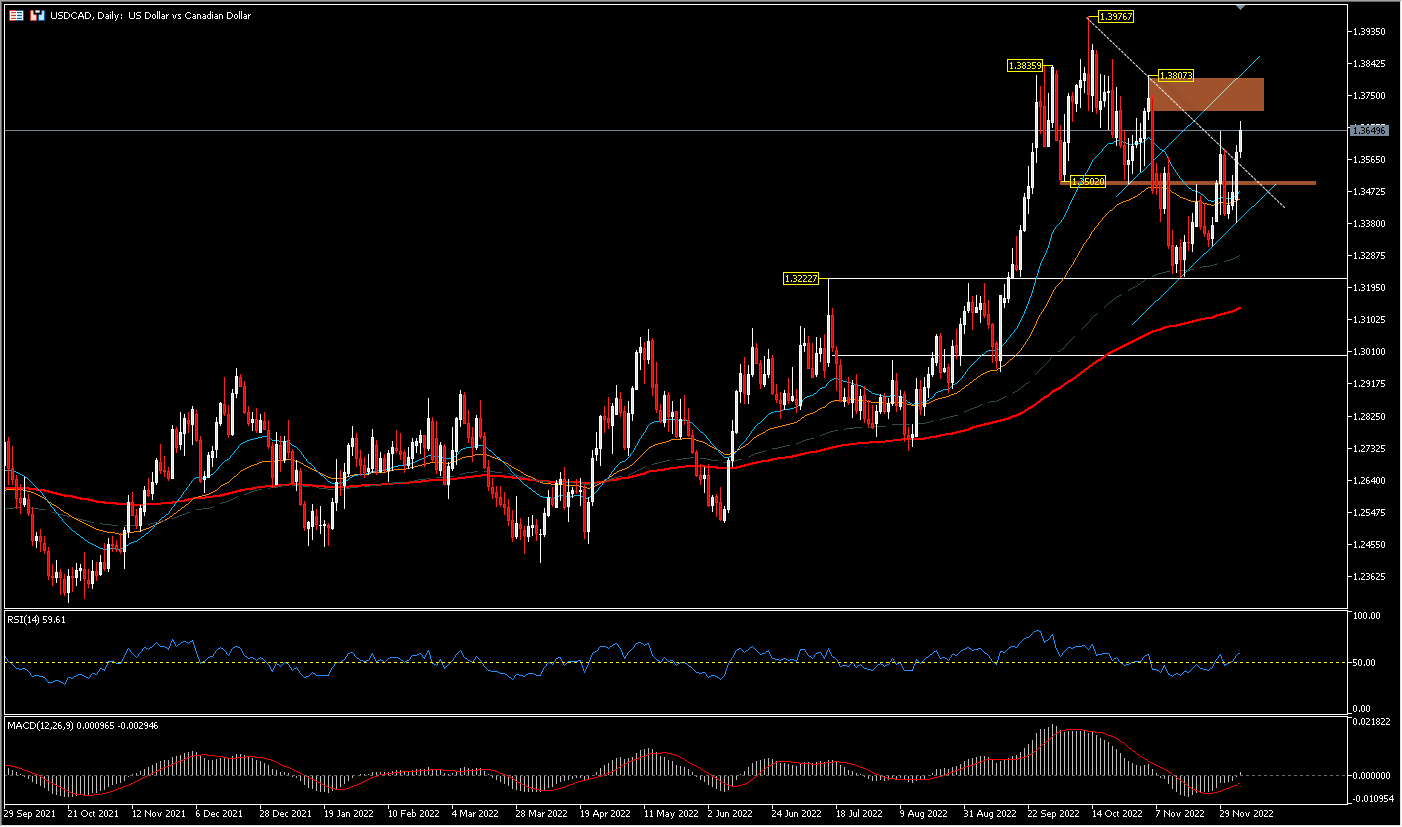

- The USD Index closed at 106.389 but had tumbled to a low of 106.28 from an overnight high of 108.44. It’s down from 112.93 on the November 3 FOMC day. Stocks extended gains at the Friday close with another solid session, albeit in choppy action amid worries over the bankruptcy of FTX. Yields – 10-year Treasury yield is up 6.7 bp at 3.88%, EGB yields are correcting from the highs seen on Friday, however the ECB remains on course to tighten rates beyond neutral and start QT next year.

- EUR – above parity at 1.0320.

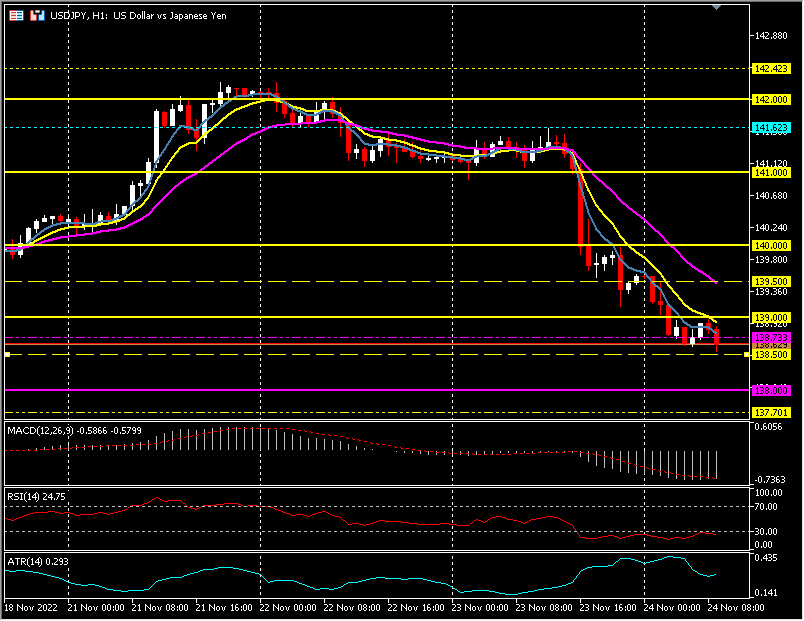

- JPY – sideways at 139.50.

- GBP – turned below 1.1800.

- Stocks – US100 to a 1.88% surge, while the US500 was up 0.92%. The US30 edged up 0.1%. The components of the US500 were mixed but a 3% pop in energy and a 2.46% jump in consumer discretionary sectors helped overcome losses in health care and utilities. Today, stocks struggled a bit and corrected some of last week’s gains, although China bourses got a boost from official directives aimed at supporting the ailing property sector, which added to the slight easing of virus restrictions that were announced last week. Hang Seng and CSI 300 are currently up 1.8% and 0.2% respectively, after Nikkei and ASX closed with losses of -1.1% and -0.2%, weighed down by financials data. GER40 and UK100 futures are up 0.2% and 0.1%.

- Reuters reported that Chinese regulators have told financial institutions to extend more support to property developers to shore up the struggling real estate sector.

- USOil – at $88.40.

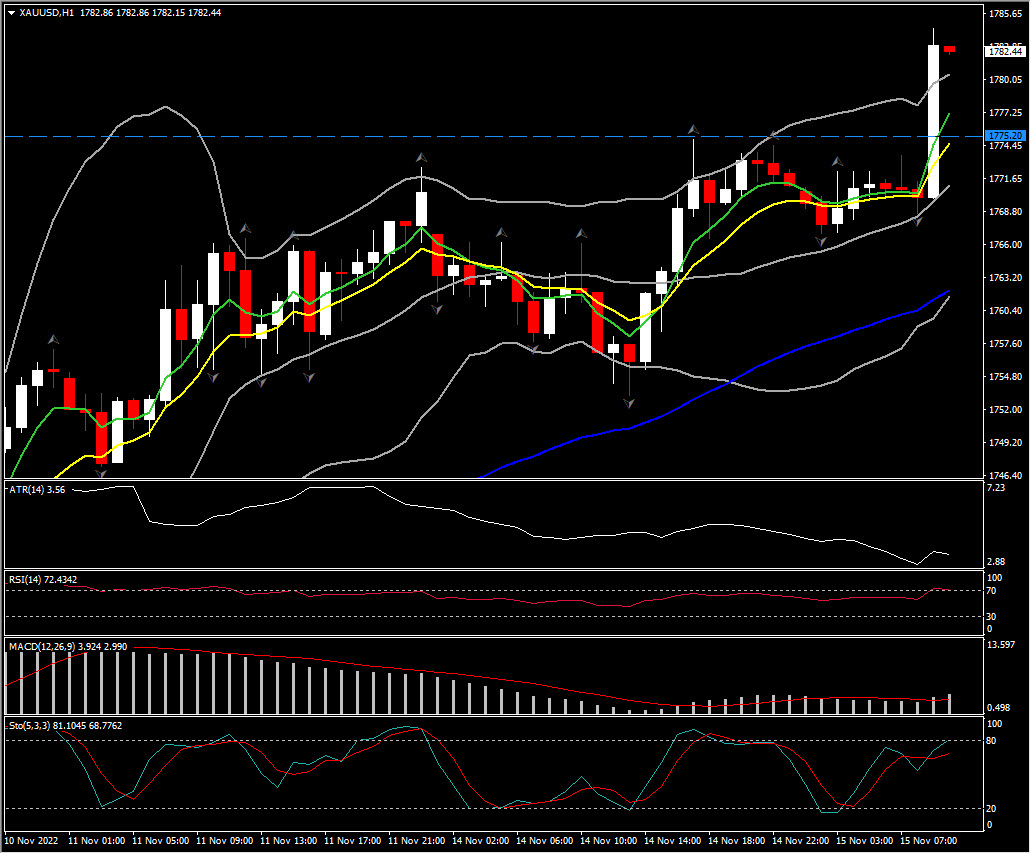

- Gold – had its best week since March, currently holds gains at 1763.

- BTC – slipping into the $16,000 area again.

Biggest FX Mover @ (06:30 GMT) BTCUSD (+1.12%) rebounded to 16890 but struggling to break 50-hour SMA. MAs aligning higher, MACD lines still negative, RSI 53 & flat indicating that this might be a limited bounce. H1 ATR 313.46, Daily ATR 1334.606.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.