HFM.

Senior member

- Messages

- 2,282

- Likes

- 0

Date : 10th October 2022.

Market Update – October 10 – Dollar Remains Bid, Stocks Weighed.

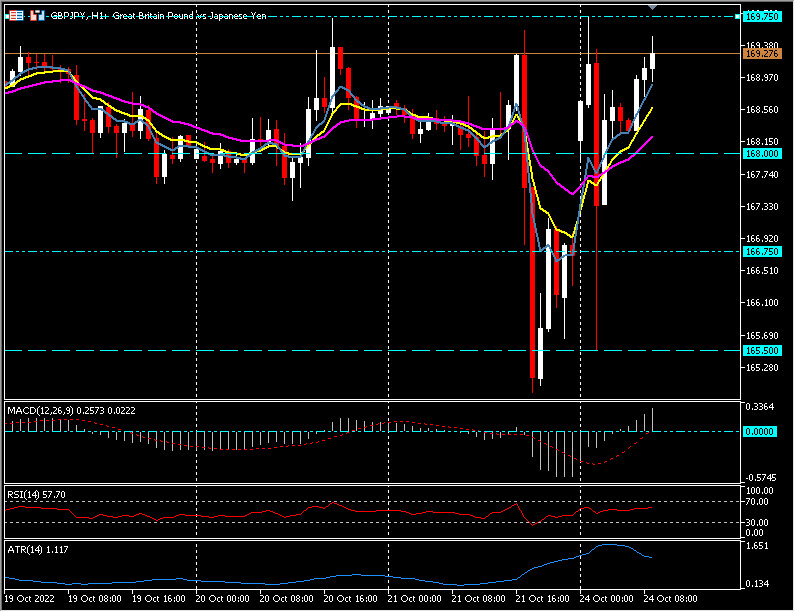

Biggest FX Mover @ (06:30 GMT) GBPAUD (+0.64%) Continued to rally from Friday’s low at 1.7350 to test 1.7500 now. MAs aligned higher, MACD histogram & signal line positive & rising, RSI 66.52 & rising, H1 ATR 0.00347, Daily ATR 0.03100.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 10 – Dollar Remains Bid, Stocks Weighed.

- USDIndex – Rallied again following strong NFP data (263k vs 250k & Unemployment falling to 3.5% from 3.7%) on Friday and expectations of no FED pivot any time soon and unified central bank action. Trades at 112.80. Yields are firmer and stocks on the back foot. US CPI key this week. Putin reaction to Bridge attack potentially Nuclear, Xi Ping looks to cement more power for another 10 years and NK have simulated attacks on SK – all under-mining sentiment. US moves to curb US chip technology to China hits Chinese hi-tech companies. Asian (thin markets due to holidays and weak Chinese Service PMI data 49.3 vs 55.0) & European stocks are lower following the very weak close (NASDAQ -3.8% ) on Wall St.

- EUR – closed Friday at 0.9730, and trades at 0.9720 now.

- JPY – rallied Friday and again today spiked to 145.60 and holds over the key 145.00 now. Signs of more BOJ intervention.

- GBP – sterling sank again too, Cable back to 1.1075 with the pressure on new PM Truss showing no signs of waning.

- Stocks – US stocks, were extremely heavy on Friday and closed down –2.11% to -3.8%. US500 -105.00 at 3639. AMD -13.87%, TSLA -6.32%, NVDA -8.03%. US FUTS at 3635.

- USOil rallied again to $93.00 and trades at $92.20 now.

- Gold – declined again as strong USD and high Yields weigh, from $1710 on Friday ahead of NFP to $1685 now.

- BTC – also weighed by weak sentiment and a strong USD sank from 20k pivot on Friday to trade at 19.3k now.

Biggest FX Mover @ (06:30 GMT) GBPAUD (+0.64%) Continued to rally from Friday’s low at 1.7350 to test 1.7500 now. MAs aligned higher, MACD histogram & signal line positive & rising, RSI 66.52 & rising, H1 ATR 0.00347, Daily ATR 0.03100.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.