You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Best Thread Correlation Trading - Basic Ideas and Strategies

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

FXCorrelator working well since early this morning ("Talking my own book"). Informed market opinion:

"Federal Reserve expected to announce today an expansion of asset purchases that tend to weaken the U.S. currency."

sounds good.............wish I could play but i'm in a wintery switzerland until saturday

later all....Hamish in the chair 👍

N

sounds good.............wish I could play but i'm in a wintery switzerland until saturday

later all....Hamish in the chair 👍

N

Regret that the Internet service was cut-ff this morning - severe frost last night? Wouldn't surprise me if the heavy boot of the 'Elf and Saf'ey Gestapo wasn't involved somewhere. Wearing googles indoors when it reaches -2 is "mandatory". When I have had a look around I'll revert. H

The Gmomes of Zurich have been re-jigging their precious Franc and bought a few billions more Euros, Helicopter Ben says the Fed's latest measures will not avert the 'fiscal cliff' so there was safety-shot buying of the greenback, the Sons of Nippon saw new lows and are happy for their exporters... on the H4 bias the NZD looks like the star perfomer; I will buy GBYUSD and GBYJPY (lots of lovely volatility) and might pick-up some EURUSD (all on a end-of-day view) when the Kiddies in the City come back to their desks after lunch. .

Hope this adds something to your day and thank-you NPV for permitting me to pontificate. Please shoot me immediately if I am misguided - but remember -

remember -"E&OE" (the great stock-brokers Get Out card)!

pip-pip and ... trade canny, Hamish

Hope this adds something to your day and thank-you NPV for permitting me to pontificate. Please shoot me immediately if I am misguided - but remember -

remember -"E&OE" (the great stock-brokers Get Out card)!

pip-pip and ... trade canny, Hamish

FXRobinson

Junior member

- Messages

- 20

- Likes

- 0

I am watching S&P 500 for EURUSD direction. Also I watch AUD and copper for risk on - risk off

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

mornin all.....

damn flight was delayed so got home 10pm last night........

ok will look at the week later on if i get time

hope people made money last week..i didnt make much as i was not at the screens much after monday

this work lark really screws up the trading !

N

damn flight was delayed so got home 10pm last night........

ok will look at the week later on if i get time

hope people made money last week..i didnt make much as i was not at the screens much after monday

this work lark really screws up the trading !

N

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

I am watching S&P 500 for EURUSD direction. Also I watch AUD and copper for risk on - risk off

nice..........I tend to not follow the commodity correlation to much although I do follow some simple Gold rules

see my other thread re my goldmeter here at T2W 👍

thanks for contributing and let us know how you are doing :smart:

N

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

hey all heres the 4Hr on a 20/3 setting.....

well any idiot trying to tip buying Yen in Q4 will have been very dissapointed (like me - see my Q4 strongest currency poll/thread !)

the Dow untl now has been damn damn resilient......but I think finally we are getting a little bit more realism in the game as we head towards the inevitable fiscal cliff climax......

N

well any idiot trying to tip buying Yen in Q4 will have been very dissapointed (like me - see my Q4 strongest currency poll/thread !)

the Dow untl now has been damn damn resilient......but I think finally we are getting a little bit more realism in the game as we head towards the inevitable fiscal cliff climax......

N

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

hey all

I had major plans to review charts and give some updates today - but a few chores and calls from the house move are still detaining me ....

will try to catch up in the week.......but we are virtually out of runway for 2012 so in truth its probably more some navel gazing for 2013 that will be the order of the day

based on my Quartus Horriblus performance of tipping the Yen - I may decide to step away from the prediction game and stick to just trading.....!

i'll close out my poll/thread soon here at t2w and see who did deliver the money in Q4.........it could be a crazy outsider ...........sorry but you will need to visit the poll/thread here to see whats happening

http://www.trade2win.com/boards/forex/160932-strongest-g8-currency-q4-competition-5.html#post2035858

see you in the trenches tomorrow for the last week of combat

N

I had major plans to review charts and give some updates today - but a few chores and calls from the house move are still detaining me ....

will try to catch up in the week.......but we are virtually out of runway for 2012 so in truth its probably more some navel gazing for 2013 that will be the order of the day

based on my Quartus Horriblus performance of tipping the Yen - I may decide to step away from the prediction game and stick to just trading.....!

i'll close out my poll/thread soon here at t2w and see who did deliver the money in Q4.........it could be a crazy outsider ...........sorry but you will need to visit the poll/thread here to see whats happening

http://www.trade2win.com/boards/forex/160932-strongest-g8-currency-q4-competition-5.html#post2035858

see you in the trenches tomorrow for the last week of combat

N

Last edited:

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

Ladies and gentlement - start your engines........

N

Economic outlook: (FT)

The Federal Reserve is expected to stick firmly on its course of monetary easing at its open market committee meeting this week, announcing further bond purchases in its continuing efforts to stimulate growth and add liquidity to financial markets.

Members of the Fed’s policy committee are expected to opt on Wednesday for further asset purchases when its maturity extension programme, “Operation Twist”, concludes at the end of the year.

EDITOR’S CHOICE

Fed set to unveil extra asset purchases - Dec-04.Companies in last-minute bond flurry - Dec-05.Muted gains for stocks after US payrolls - Dec-07..The central bank voted at its last meeting in October to continue monthly purchases of $40bn in mortgage backed assets, but the minutes of that meeting suggested there were growing calls to supplement these purchases with outright buying of Treasury bonds once “Twist” ends.

“The Fed has indicated that it will continue QE3 until there is a substantial improvement in the labour market. This is probably still a long way off,” says John Higgins at Capital Economics.

Most analysts believe the Fed will add about $45bn a month in Treasury purchases, leaving total monthly asset buying at $85bn, while it is also expected to maintain its view that the Fed Funds rate should remain at, or close to, zero until at least mid-2015.

Meanwhile, on Thursday, the Swiss National Bank is expected to keep its main target rate at between zero and 0.25 per cent and reiterate its policy of keeping a lid on the franc at SFr1.20 per euro. Most analysts expect this policy to remain in place throughout 2013.

The main focus in the UK will be Wednesday’s unemployment data. The downward revision of growth forecasts and the subsequent extension of austerity measures highlighted in the government’s Autumn Statement suggest that the unemployment rate, which in September stood at 7.8, has not peaked for the year.

The British Chambers of Commerce last week predicted the rate would hit 8.1 per cent in the fourth quarter, and the consensus view of analysts see it rising to 7.9 per cent in October.

October trade data from three of the world’s biggest economies is published this week, with China and Germany seen reporting narrowing trade surpluses, although both are expected to report some improvement in exports. In the US on Tuesday, the trade deficit is expected to widen to $42bn in October from $41.5bn the previous month.

The main events for the eurozone this week are the European Council and Ecofin meetings, the latter on Wednesday to further discuss banking supervision and hopefully to approve disbursement of Greek aid.

Economic data remains grim, but the rate at which business activity is slowing in the eurozone is expected to moderate. The preliminary readings on eurozone purchasing manager indices for this month, released on Thursday, are forecast to see the manufacturing index climb to 46.4 from 46.2 in November, while services is seen rising to 47.1 from 46.7. A reading above 50 indicates economic growth in the sector.

“Both indices will continue to indicate falling levels of activity, which would be consistent with our forecast for the recession to have extended through to the end of the year,” said James Ashley at RBC Capital Markets.

N

Economic outlook: (FT)

The Federal Reserve is expected to stick firmly on its course of monetary easing at its open market committee meeting this week, announcing further bond purchases in its continuing efforts to stimulate growth and add liquidity to financial markets.

Members of the Fed’s policy committee are expected to opt on Wednesday for further asset purchases when its maturity extension programme, “Operation Twist”, concludes at the end of the year.

EDITOR’S CHOICE

Fed set to unveil extra asset purchases - Dec-04.Companies in last-minute bond flurry - Dec-05.Muted gains for stocks after US payrolls - Dec-07..The central bank voted at its last meeting in October to continue monthly purchases of $40bn in mortgage backed assets, but the minutes of that meeting suggested there were growing calls to supplement these purchases with outright buying of Treasury bonds once “Twist” ends.

“The Fed has indicated that it will continue QE3 until there is a substantial improvement in the labour market. This is probably still a long way off,” says John Higgins at Capital Economics.

Most analysts believe the Fed will add about $45bn a month in Treasury purchases, leaving total monthly asset buying at $85bn, while it is also expected to maintain its view that the Fed Funds rate should remain at, or close to, zero until at least mid-2015.

Meanwhile, on Thursday, the Swiss National Bank is expected to keep its main target rate at between zero and 0.25 per cent and reiterate its policy of keeping a lid on the franc at SFr1.20 per euro. Most analysts expect this policy to remain in place throughout 2013.

The main focus in the UK will be Wednesday’s unemployment data. The downward revision of growth forecasts and the subsequent extension of austerity measures highlighted in the government’s Autumn Statement suggest that the unemployment rate, which in September stood at 7.8, has not peaked for the year.

The British Chambers of Commerce last week predicted the rate would hit 8.1 per cent in the fourth quarter, and the consensus view of analysts see it rising to 7.9 per cent in October.

October trade data from three of the world’s biggest economies is published this week, with China and Germany seen reporting narrowing trade surpluses, although both are expected to report some improvement in exports. In the US on Tuesday, the trade deficit is expected to widen to $42bn in October from $41.5bn the previous month.

The main events for the eurozone this week are the European Council and Ecofin meetings, the latter on Wednesday to further discuss banking supervision and hopefully to approve disbursement of Greek aid.

Economic data remains grim, but the rate at which business activity is slowing in the eurozone is expected to moderate. The preliminary readings on eurozone purchasing manager indices for this month, released on Thursday, are forecast to see the manufacturing index climb to 46.4 from 46.2 in November, while services is seen rising to 47.1 from 46.7. A reading above 50 indicates economic growth in the sector.

“Both indices will continue to indicate falling levels of activity, which would be consistent with our forecast for the recession to have extended through to the end of the year,” said James Ashley at RBC Capital Markets.

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

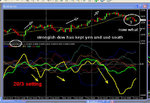

ok here we are

the left chart is 4hr on a 20/3 setting ...the strength order of the currencies gives me a longer term bias for picking the shorter TF trades..and i should only trade pairs in direction of the rankings

so at the moment its all about (still) selling the yellow yen and also the green usd (and the CAD)....and the Blue EURO continues to be the number 1 draft buy choice

like last night as the Euro bounced north and Yen got sunk........middle is a 15m TF 20/1 setting ..normal FXCorrelator settings

and as you can see onthe right side .........that E/J has been a peach since mid Dec ........even off of a recently bearish Dow .....amazing !

trade what you see today on lower TF's but you have been warned here about the best trades by looking at that 4hr bias setting ...........

N

the left chart is 4hr on a 20/3 setting ...the strength order of the currencies gives me a longer term bias for picking the shorter TF trades..and i should only trade pairs in direction of the rankings

so at the moment its all about (still) selling the yellow yen and also the green usd (and the CAD)....and the Blue EURO continues to be the number 1 draft buy choice

like last night as the Euro bounced north and Yen got sunk........middle is a 15m TF 20/1 setting ..normal FXCorrelator settings

and as you can see onthe right side .........that E/J has been a peach since mid Dec ........even off of a recently bearish Dow .....amazing !

trade what you see today on lower TF's but you have been warned here about the best trades by looking at that 4hr bias setting ...........

N

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

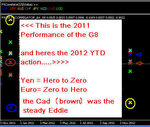

I was just looking back at the years performance.........verses 2011

heres the x-men showing the positions.........

Yen is a rollercoaster........it was by far the buy in 2011....but went from hero to zero this year.....and Euro was the opposite

c'mon be honest........Euro may still be the strongest performing G8 currency in 2012 , and who in the hell would have called that this time last year ?

the fund managers have an equity trading system around buying Dogs and selling the stars of the previous periods results........(annual , quarterly) seems like we might start doing that on the G8 ?

it would have yielded some 10% this year on simply reversing that Yen/Euro position from Dec 2011 results

N

heres the x-men showing the positions.........

Yen is a rollercoaster........it was by far the buy in 2011....but went from hero to zero this year.....and Euro was the opposite

c'mon be honest........Euro may still be the strongest performing G8 currency in 2012 , and who in the hell would have called that this time last year ?

the fund managers have an equity trading system around buying Dogs and selling the stars of the previous periods results........(annual , quarterly) seems like we might start doing that on the G8 ?

it would have yielded some 10% this year on simply reversing that Yen/Euro position from Dec 2011 results

N

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

hey all..........jees just realised we hit the 450,000 views last week

this is the forex thread hall of fame viewing figures......attached

and i'm proud to be in that company of threads there :smart:

Many thanks to everyone and I hope the thread has been of some help to people in understanding the potential of using strengthmeters in your trading 👍

N

this is the forex thread hall of fame viewing figures......attached

and i'm proud to be in that company of threads there :smart:

Many thanks to everyone and I hope the thread has been of some help to people in understanding the potential of using strengthmeters in your trading 👍

N

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

been chasing the E/U scalps......hard work as I was hoping the USD would be a little firmer here....................E/J was the easier play it seems so far

N

(yes - its against the 4hr bias signals but I never follow my own rules unless it suits me .....hahahahaha 😎)

N

(yes - its against the 4hr bias signals but I never follow my own rules unless it suits me .....hahahahaha 😎)

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

aside from the scalps.............(well my view of the scalps)

watch the GBP..........its strong and its strength is being hidden by the Dow weakness/Yen strength at the moment ........ 😎

definately the play if dow rallies and this time the trade would be with the 4hr bias signal 👍

i suspect many scalpers are already buying G/U anyway agead of the move

N

watch the GBP..........its strong and its strength is being hidden by the Dow weakness/Yen strength at the moment ........ 😎

definately the play if dow rallies and this time the trade would be with the 4hr bias signal 👍

i suspect many scalpers are already buying G/U anyway agead of the move

N

Attachments

NVP

Guest Author

- Messages

- 37,968

- Likes

- 2,158

aside from the scalps.............(well my view of the scalps)

watch the GBP..........its strong and its strength is being hidden by the Dow weakness/Yen strength at the moment ........ 😎

definately the play if dow rallies and this time the trade would be with the 4hr bias signal 👍

i suspect many scalpers are already buying G/U anyway agead of the move

N

hard work scalping but it is happening for GU.........👍

E/U may deliver as well.......

N

Attachments

Similar threads

- Replies

- 0

- Views

- 4K