Alpha Pro Tech - Quantifying The Substantial Upside

Oct. 1, 2020 2:33 PM ET

|

8 comments

|

About:

Alpha Pro Tech, Ltd. (APT)

Florian Buschek

Long/Short Equity, Growth At Reasonable Price, long-term horizon, small-cap

(93 followers)

Summary

The supply/demand picture for N95 masks is extremely bullish short to midterm.

I explicitly model the up- and downsides based on N95 sales projections and inferred gross margins.

60% upside is my base case.

I see no downside at the current share price.

Alpha Pro Tech (NYSEMKT:

APT) has been a strong performer this due to the extremely elevated demand for N-95 respirators to protect people against COVID-19. It seems that the market has decided this was all hype and all that demand will quickly go away, sending APT's earnings and stock price back to earth.

In this piece I will argue against that narrative and make the case why APT is drastically undervalued with very low downside risk based on my model comprising N95 sales and the other business lines.

Business

Alpha Pro Tech manufactures and sells disposable protective apparel and building supply products in the United States and internationally. The two segments are Building Supply and Disposable Protective Apparel.

The Building Supply segment consists of construction weatherization products, such as housewrap and synthetic roof underlayment as well as other woven material.

The Disposable Protective Apparel segment is comprised of disposable protective garments (including shoecovers, bouffant caps, coveralls, gowns, frocks and lab coats), face masks and face shields. The most prominent part and the center of my analysis are the NIOSH (National Institute for Occupational Safety and Health) approved N-95 Particulate Respirators.

It is important to note the APT's N95s are of extremely high quality. From conversations with practitioners, they are more comfortable to wear, easier to fit properly and ironically of much higher quality than 3M's N95s (ironically because the first masks of this kind were

released by 3M). Because of this qualitative advantage, the masks APT produces are in high demand but basically unavailable for retail buying, instead the company has sold all its capacity into contracts and larger institutions.

Supply and Demand Picture

The important point to understand about N95 masks is that in contrast to simple cloth masks, they do protect both the persons wearing them and the outside world. There is a cheaper and more available version called KN95, but these are not NIOSH approved and

do not offer full protection

The general demand picture is very robust for the N95 masks market valued at

US$ 2.2B in 2019. Specifically, in the acute fight against COVID-19 there is an extreme shortfall of N95s.The following

excerpts illustrate the severity of this supply/demand-imbalance:

'Even though we are making more respirators than ever before and have dramatically increased production,' 3M spokeswoman Jennifer Ehrlich said, 'the demand is more than we, and the entire industry, can supply for the foreseeable future.'

Still, hospitals and other entities, including state governments, are having nearly as much difficulty obtaining N95s as they did early in the pandemic.

The article goes on to describe the situation in Minnesota as an example, where the state has orders for more than 5 million N95s for hospitals, but has received only 337,000 masks so far through traditional 3M distributors. Here's

further evidence for unfulfilled demand:

Critical shortfalls of medical N95 respirators - commonly referred to as N95 masks - and other protective gear started in March, when the pandemic hit New York. Pressure on the medical supply chain continues today, and in 'many ways things have only gotten worse,' the American Medical Association's president, Dr. Susan Bailey, said in a recent statement.

But today, hospital administrators - some of whom are facing new state orders to stockpile supplies - say they can't get as many masks as they want, and the FDA included N95s on its most recent medical supply shortage list.

Now even if there was enough supply for today's demand, demand itself is not fixed at all and in reality much higher. The reason is that current respirators are

used for far too long and reused too frequently.

N95s were designed to be thrown away after every patient. By this July afternoon, Williams had been wearing the same one for more than two months.

The survey asked whether nurses were still experiencing shortages of personal protective equipment, or PPE. The answer was a resounding yes. 'A third reported that they were out of or short of N95 respirators. Almost 60% of the nurses surveyed said they're re-using single-use protective equipment for five or more days, and 68% said their facilities mandate re-using the supplies,' Bloomberg reported.

Nurses are especially

exposed to this issue and we can be sure that hospitals will need large numbers of N95s as long as we have deal with the virus:

'Re-use and decontamination of single-use personal protective equipment as the "new normal" is unacceptable, given the lack of standards and evidence of safety,' ANA President Ernest Grant, Ph.D., RN, FAAN, said Tuesday in a statement announcing the survey findings.

The association queried more than 21,000 nurses between July 24 and Aug. 14. Fully 68% of reported that their facility requires reuse of single-use PPE, such as N95 masks. Most said they are reusing masks for at least five days if not more, with that number growing by 15% by August. When asked whether they felt unsafe reusing masks, 62% of respondents in August said that they did, and more than half (53%) reported feeling unsafe using the equipment after decontamination.

This is an emergency solution, but it's clearly not sustainable since it can

cause significant harm. There will also be additional demand from private households and retail as soon as more N95s are actually available. Finally, the rebuilding of national stockpiles will take years and I would be very surprised if the size of these stockpiles was not increased for good to be better prepared for the next pandemic. (It should be noted that N95s have a

finite shelf life and thus maintaining the stockpile will require continued supply)

All these factors are pointing to continued demand for years. So why are current producers not doubling and tripling their capacity again and again? After all, 3M (NYSE:

MMM) is

well on track to do so expecting to produce 2 billion respirators globally, more than a threefold increase versus 2019.

The answer is

twofold: Existing producers don't want to invest for peak demand and don't share their IP:

Ask the PPE industry and the refrain is that without long-term guarantees that the government will keep buying respirators, N95 manufacturers are wary of investing too much, and other companies that could start making respirators or the filters for them are hesitant to do so.

Peter Tsai, the scientist who invented a method to charge the fibers inside the respirator filter, knows why: 'It is not profitable to make respirators in the United States,' he said. It can take six months just to create one manufacturing line that makes the N95′s filter.

'Folks aren't likely to share that information outside of their own company,' said Jeff Peterson, who now oversees NIOSH approvals. NIOSH employees may know how 3M makes its respirators and the filters inside them. But by contract, they can't tell other manufacturers how to do the same.

Projections and Financials

The company currently produces N95s in one production line and is bringing its phase 2 expansion online with first production in the current quarter. Clearly the previous sales and production numbers have disappointed, but the underlying issues, namely supply

bottlenecks are fixed.

The total production capacity for fiscal 2021 will be over $100 million, which is very small compared to 3M for example. This is clearly a benefit, since customers will want to diversify their sources so that we can be sure that APT will be able to keep selling their capacity and compete effectively. Management is very confident that all the capacity will be needed. One could ask why there is not more in orders or backlog already. The reason is that mgmt. acted prudent and only took on orders that they were absolutely sure they could fulfil. In my eyes this is commendable and increases trust in APT as reliable supplier.

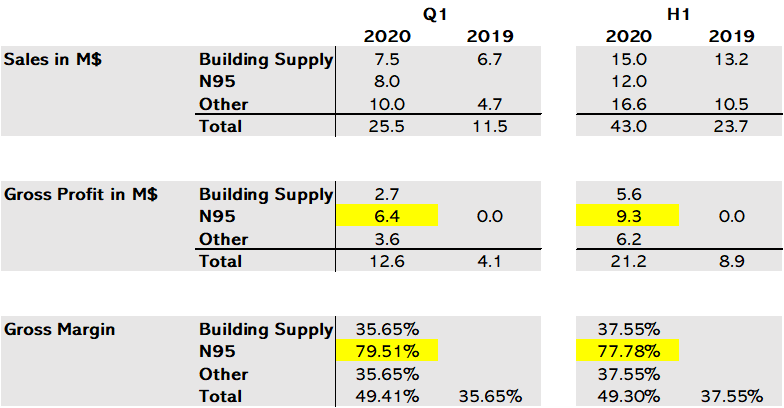

Based on the

recent PR we can deduce that $31 million of booked N-95 face mask orders will be fulfilled in H2 2020. A key question is what margin the company is achieving for its respirators. This is not disclosed but we can roughly infer it from historical gross margins predominantly from building supply and other protective apparel and most recent gross margins. The following image demonstrates this for Q1 2020 compared to 2019 and for a consistency check likewise for H1. We know 2019 gross margins of 35.65% and 37.55% and can apply them to the sales lines for building supply and other in 2020. From that we get the gross profit attributable to these items and can back out the gross profit form N95 sales and the respective gross margins, highlighted in yellow. This is an approximation but provides reasonable guidelines.

Source: Own work based on historical financials

The resulting gross margins of 77-80% are extraordinary, essentially software type economics. Of course considering the severe supply shortfall it is not surprising. However, it would be foolish to assume these margins to be sustainable, it is just not realistic that these margins would not be negotiated down once supply catches up or competed away. Therefore, in my model I will assume a decline in 10% increments every year after 2021 while holding sales fixed at $105M. Talking to management, they don't expect stockpiling even to begin until at least 2022 and then last until 2025 based on private forecasts. Thus I will model explicitly until 2025. I keep operating expenditure fixed at the annualized H1 2019 level and assume a tax rate of 20%. Instead of calculating the WACC I choose my personal discount rate of 10% and use the perpetuity value for 2025ff. The resulting NPV per share is $13.38 for the N95 part only.

Source: Own work

All other segments are growing as well, due to elevated demand for other protective gear and the housing supply should benefit from the recent strength in home sales. But I will make my life easy and simply take the gross profit of $9M from H1 2019 and add it annualized to the gross profit from N95s in every year. This is very conservative as it assumes no growth at all.

Source: Own work

The resulting NPV is $24.62, a 62% return from today's share price of about $15.

Put differently, in order to get to the current share price, we need a discount rate of 23%. That means, according to this projection, we can expect an annual rate of return of 23% forever, if we buy at the price that is currently offered.

Source: Own work

This doesn't even include the $1.8 cash per share that is currently on the balance sheet. Astute readers will notice that I haven't discounted cash flows, but earnings. This is justified because the business model is not very capital intensive while net income and free cash flow (cash flow from operations - capex) have either tracked each other very closely on a normalized basis or free cash flow has vastly exceeded net income.