CompoundTrader

Newbie

- Messages

- 6

- Likes

- 0

Hi trade2win, I've been involved with trading for several years and have been working full time on building a trading strategy since last October.

I have started live simulation trading this January, but the results are not good enough yet. I am looking for some guidance on how to use maths and statistics to identify when I am ready to go live.

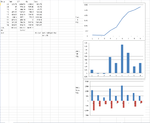

Here is the last two weeks (date, net profit, gross profit, gross loss, cumulative net profit):

The statistics I am tracking so far:

-profit factor (ratio of gross loss to gross profit)

-ratio of net profit to maximum drawdown

-gross losses

The reason I am choosing these statistics is that I want to focus on keeping my losses as small as possible in order to use leverage effectively and compound my account. I believe if I prepare properly, total risk can be kept small, so I plan on starting with a $4,000 futures account and staking $10/tick.

Profit factor tells me how many dollars I earn for each dollar lost, and I would like this to be 3 or more. Also, in any rolling 5 day period, I want to have made at least 4x my maximum drawdown in that period. Both of these together will ensure that time to recovery after drawdown is as quick as possible.

Total gross losses are still far too high. There are various improvements I can make to my method to eliminate some of these losses. This will take time - the question is, when am I successful enough to begin live trading?

My question for trade2win is are there any other measurements I should be using to track how consistent I am, how much risk I am taking, and therefore what leverage to use? I have read about Kelly, but doesn't really apply as I am starting trading with 1 contract - cannot go smaller or larger than this with my initial risk capital. And I will need to double my trading size to 2 contracts at some stage, without having out of proportion losses at the new size. After this, compounding should be lower risk due to being able to add smaller increases in size (2 to 3 contracts, 3 to 4 etc).

I am always paying the spread on my simulation account and these results include the commissions and fees I will pay when live.

I don't plan on going live until I know with high probability I can compound without ever drawing down more than 50% of total account equity.

How do traders here approach statistics and position sizing?

I have started live simulation trading this January, but the results are not good enough yet. I am looking for some guidance on how to use maths and statistics to identify when I am ready to go live.

Here is the last two weeks (date, net profit, gross profit, gross loss, cumulative net profit):

The statistics I am tracking so far:

-profit factor (ratio of gross loss to gross profit)

-ratio of net profit to maximum drawdown

-gross losses

The reason I am choosing these statistics is that I want to focus on keeping my losses as small as possible in order to use leverage effectively and compound my account. I believe if I prepare properly, total risk can be kept small, so I plan on starting with a $4,000 futures account and staking $10/tick.

Profit factor tells me how many dollars I earn for each dollar lost, and I would like this to be 3 or more. Also, in any rolling 5 day period, I want to have made at least 4x my maximum drawdown in that period. Both of these together will ensure that time to recovery after drawdown is as quick as possible.

Total gross losses are still far too high. There are various improvements I can make to my method to eliminate some of these losses. This will take time - the question is, when am I successful enough to begin live trading?

My question for trade2win is are there any other measurements I should be using to track how consistent I am, how much risk I am taking, and therefore what leverage to use? I have read about Kelly, but doesn't really apply as I am starting trading with 1 contract - cannot go smaller or larger than this with my initial risk capital. And I will need to double my trading size to 2 contracts at some stage, without having out of proportion losses at the new size. After this, compounding should be lower risk due to being able to add smaller increases in size (2 to 3 contracts, 3 to 4 etc).

I am always paying the spread on my simulation account and these results include the commissions and fees I will pay when live.

I don't plan on going live until I know with high probability I can compound without ever drawing down more than 50% of total account equity.

How do traders here approach statistics and position sizing?