A handy simulator that , thanks Glenn.

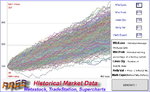

The attachment shows 1000 possible outcomes of a system that wins 36% of the time with a 2.75 average win:loss ratio.

I assume you start with 100 units then on each trade you either win 2.75 or lose 1.

I am having a mental block as to how to fit this to real world futures trading. Imagine a system with these results that trades once a day for approx 2 years and assume this results in exactly the 453 trades shown.

The return on 100 units seems to vary between approx 30% and 267% (130 to 397 units)

How do I translate the percentage increase into, say, pips per day or return on original capital given that futures involve leverage? What other variables do I need? Is this a complex calculation or am I missing something obvious?

Thanks very much.