The reverse calendar spread is not neutral and can generate a profit if the underlying makes a huge move in either direction. The risk lies in the possibility of the underlying going nowhere, whereby the short-term option loses time-value more quickly than the long-term option, which leads to a widening of the spread, exactly what is desired by the neutral calendar spreader. Having covered the concept of a normal and reverse calendar spread, let's apply the latter to S&P call options.

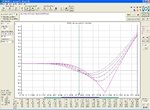

At volatile market bottoms, the underlying is least likely to remain stationary over the near-term, which is an environment in which I like to use reverse calendar spreads; furthermore, there is a lot of implied volatility to sell, which, as mentioned above, adds profit potential. The details of our hypothetical trade are presented in figure 1 below.

http://www.investopedia.com/articles/optioninvestor/02/081902.asp

What will happen if S&P futures continues to fall and Implied Volatility increases?

At volatile market bottoms, the underlying is least likely to remain stationary over the near-term, which is an environment in which I like to use reverse calendar spreads; furthermore, there is a lot of implied volatility to sell, which, as mentioned above, adds profit potential. The details of our hypothetical trade are presented in figure 1 below.

http://www.investopedia.com/articles/optioninvestor/02/081902.asp

What will happen if S&P futures continues to fall and Implied Volatility increases?