Grey1

Senior member

- Messages

- 2,190

- Likes

- 210

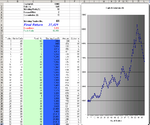

This EXCEL program should shed some light on reward/Risk/pos size/Equity curve and many more..

Risk % is the percent of your total capital you are using in each trade

Win prob is your strategy .. Dont kid yourself most traders have less that 50% system.. I sugges you use 40% for your strategy ..

Reward/risk // lets say your stop is 10 points on DOW then your exit must be 20 points to give you a 20/10 = 2 of reward/Risk

Once you have filled all cells then keep clicking on F9 to see the effect of your inputs on your capital ..

You will learn a lot by just playing with this EXCEL prog..

Risk % is the percent of your total capital you are using in each trade

Win prob is your strategy .. Dont kid yourself most traders have less that 50% system.. I sugges you use 40% for your strategy ..

Reward/risk // lets say your stop is 10 points on DOW then your exit must be 20 points to give you a 20/10 = 2 of reward/Risk

Once you have filled all cells then keep clicking on F9 to see the effect of your inputs on your capital ..

You will learn a lot by just playing with this EXCEL prog..