Ultima markets

Active member

- Messages

- 132

- Likes

- 0

US-China Agree to 90-Day Tariff Pause, CPI In Focus Next

On May 12, 2025, the United States and China concluded a two-day trade dialogue in Switzerland and reached a significant agreement: both sides will suspend certain tariffs for 90 days and implement mutual tariff reductions of 115%. This marks the first major step toward easing tensions and opening the door for broader discussions on economic and trade issues.

As part of the agreement, the U.S. will lower tariffs on Chinese imports from 145% to 30%, while China will reduce tariffs on U.S. goods from 125% to 10%. The 90-day pause provides a window for continued negotiations aimed at addressing deeper structural differences.

In addition, both countries have agreed to establish a permanent dialogue mechanism, with high-level representatives appointed to maintain regular communication and help prevent future escalations.

Market Reaction: Equities Market Gain on Optimism

The positive comments and the joint statement release by both nation after the two-day talks has sparked an optimism in global market. U.S. Stock market climbed with the S&P500 extend further gain, and Nasdaq 100 regain above the 20,000 mark on Monday. Meanwhile the China A50 also extending into the third day gain on yesterday.

This is good, but investors may still need to remain cautious during the 90-day window and the challenge of enforcing the new term still may pose risk, volatility could resurface if talks stall or a solid progress is lacking between the two world largest economies.

Still, the positive offers much-needed relief for investors, which has been rattled since the tariff announced in April 2.

CPI Data in Focus: What It Means for Markets

Even though the US and China have made progress in trade talks, a 30% tariff is still in place, and deals with other countries are still uncertain. Because of this, higher tariffs since April are still a concern for the economy.

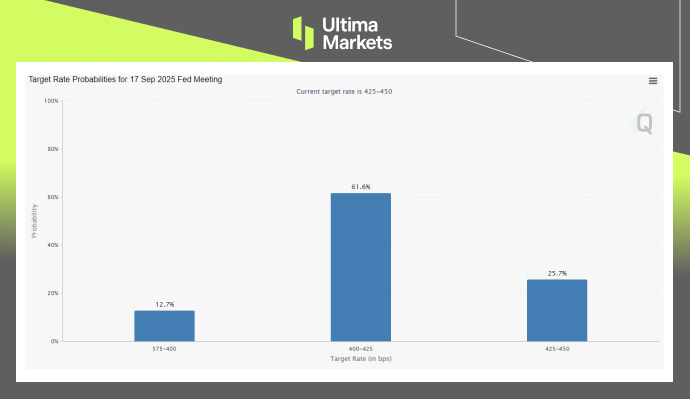

Today’s US Consumer Price Index (CPI) report is an important one. Investors want to see if higher tariffs have pushed up inflation.

If inflation is higher than expected, the Fed may keep interest rates high for longer. That could be bad news for the economy and the stock market. On the flip side, if the CPI comes in lower, markets may hope for earlier rate cuts from the Fed—good news for stocks.

Technical Outlook: SP500 & US Dollar Index

Both the US Dollar and SP500 Index see upside after the promising outlook, reversing the market pessimism earlier when Trump announced the tariff in April, which raise market losing confident in both.

US Dollar Regains 100-Mark

The US Dollar Index (USDX) has bounced after holding firmly above the key 100 level, signaling a possible bullish reversal. It’s now testing resistance around 101.30.

.jpg")

(USDX+, 4-H Chart Analysis | Source: Ultima Market MT5)

If tonight’s CPI data comes in lower than expected, it could raise hopes for Fed rate cuts—putting short-term pressure on the dollar. However, as long as the index stays above 100, the broader outlook remains positive, and the bullish setup could stay intact.

Upside Intact, Watch for Technical Pullback

The SP500 has broken above the 5800 level, confirming a bullish outlook. A softer CPI print could boost hopes for earlier Fed rate cuts, which would support further upside in equities.

.jpg")

(SP500+, Daily Chart | Source: Ultima Market MT5)

However, despite the positive momentum, a short-term technical pullback may occur—offering a potential buy-the-dip opportunity in the uptrend.

Tonight’s U.S. Consumer Price Index (CPI) release may introduce volatility across markets, particularly if the data significantly deviates from expectations.

A stronger-than-expected inflation reading could renew concerns about the longer-term impact of tariffs, potentially putting pressure on both the U.S. Dollar and equity markets. Conversely, a softer or in-line print would likely be welcomed by investors, supporting the current risk sentiment and allowing the recent market momentum to continue.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

On May 12, 2025, the United States and China concluded a two-day trade dialogue in Switzerland and reached a significant agreement: both sides will suspend certain tariffs for 90 days and implement mutual tariff reductions of 115%. This marks the first major step toward easing tensions and opening the door for broader discussions on economic and trade issues.

As part of the agreement, the U.S. will lower tariffs on Chinese imports from 145% to 30%, while China will reduce tariffs on U.S. goods from 125% to 10%. The 90-day pause provides a window for continued negotiations aimed at addressing deeper structural differences.

In addition, both countries have agreed to establish a permanent dialogue mechanism, with high-level representatives appointed to maintain regular communication and help prevent future escalations.

Market Reaction: Equities Market Gain on Optimism

The positive comments and the joint statement release by both nation after the two-day talks has sparked an optimism in global market. U.S. Stock market climbed with the S&P500 extend further gain, and Nasdaq 100 regain above the 20,000 mark on Monday. Meanwhile the China A50 also extending into the third day gain on yesterday.

This is good, but investors may still need to remain cautious during the 90-day window and the challenge of enforcing the new term still may pose risk, volatility could resurface if talks stall or a solid progress is lacking between the two world largest economies.

Still, the positive offers much-needed relief for investors, which has been rattled since the tariff announced in April 2.

CPI Data in Focus: What It Means for Markets

Even though the US and China have made progress in trade talks, a 30% tariff is still in place, and deals with other countries are still uncertain. Because of this, higher tariffs since April are still a concern for the economy.

Today’s US Consumer Price Index (CPI) report is an important one. Investors want to see if higher tariffs have pushed up inflation.

If inflation is higher than expected, the Fed may keep interest rates high for longer. That could be bad news for the economy and the stock market. On the flip side, if the CPI comes in lower, markets may hope for earlier rate cuts from the Fed—good news for stocks.

Technical Outlook: SP500 & US Dollar Index

Both the US Dollar and SP500 Index see upside after the promising outlook, reversing the market pessimism earlier when Trump announced the tariff in April, which raise market losing confident in both.

US Dollar Regains 100-Mark

The US Dollar Index (USDX) has bounced after holding firmly above the key 100 level, signaling a possible bullish reversal. It’s now testing resistance around 101.30.

(USDX+, 4-H Chart Analysis | Source: Ultima Market MT5)

If tonight’s CPI data comes in lower than expected, it could raise hopes for Fed rate cuts—putting short-term pressure on the dollar. However, as long as the index stays above 100, the broader outlook remains positive, and the bullish setup could stay intact.

Upside Intact, Watch for Technical Pullback

The SP500 has broken above the 5800 level, confirming a bullish outlook. A softer CPI print could boost hopes for earlier Fed rate cuts, which would support further upside in equities.

(SP500+, Daily Chart | Source: Ultima Market MT5)

However, despite the positive momentum, a short-term technical pullback may occur—offering a potential buy-the-dip opportunity in the uptrend.

Tonight’s U.S. Consumer Price Index (CPI) release may introduce volatility across markets, particularly if the data significantly deviates from expectations.

A stronger-than-expected inflation reading could renew concerns about the longer-term impact of tariffs, potentially putting pressure on both the U.S. Dollar and equity markets. Conversely, a softer or in-line print would likely be welcomed by investors, supporting the current risk sentiment and allowing the recent market momentum to continue.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.