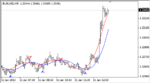

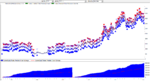

Real time testing my NN indicator (GA on NST used to find best parameter) recently

Take too long for me to upload this video here😱

Then I placed on this link

eurusd5m test video - Download - 4shared

Anyone an see the actual result eurusd now

Take too long for me to upload this video here😱

Then I placed on this link

eurusd5m test video - Download - 4shared

Anyone an see the actual result eurusd now