Hi Clarod,

Yes you can send it to me, preferred if you can send the c code, I would compare it the formula given by Ehler. I found inside mq4 code:

if (NumOfBars < 7)

{

Smooth= (iMA(NULL,0,1,0,0,Price,i) + (2*iMA(NULL,0,1,0,0,Price,i+1)) + (2*iMA(NULL,0,1,0,0,Price,i+2)))/4;

}

Smooth= (iMA(NULL,0,1,0,0,Price,i) + (2*iMA(NULL,0,1,0,0,Price,i+1)) + (2*iMA(NULL,0,1,0,0,Price,i+2)) + iMA(NULL,0,1,0,0,Price,i+3))/6;

Itrend= (alpha - alpha*alpha/4) * Smooth+ 0.5*alpha*alpha*Smooth[i+1] - (alpha-0.75*alpha*alpha)*Smooth[i+2] + 2*(1 - alpha)*Itrend[i+1] - (1 - alpha)*(1 - alpha)*Itrend[i+2];

Trigger= Itrend[i+1];

}

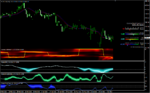

About corona, I am not sure if we can show the corona in NST. I have sample in MT4, if you have the formula and implement it on C then you can create dll file.

Here I shown Itrend and corona in MT4