ive been reading alot on here that indicators have no proven edge and ta is nonsense. Im a realist and i tend to agree with the above. I would say though that cycle analysis in multi timeframe can be used to find exhaustion points and i feel the results below prove there is infact a small edge.

Pedro pete helped me program the following code about 18 months ago, since then ive had alot of stuff added to it which has improved performance.

No one seems to make money trading, not consistantly anyway, but i feel this is because you have to view it from another angle and not expect to win everyday and also ive found to smooth equity curve there is needs to be a few systems running or you make money from your job/business to counter act bad weeks, imo.

I have many many parameters, and below is not cherry picked and is far from the best performance report, i just posted a realistic tradeable report to get your opinions, this way im being true to myself and getting some real feedback.

I have gone through the code and tested for errors at every step possible in live real time, there is no bugs at present. I have added some realistic slippage to all trades, I have added comms. Execution is of course another matter and one i will feel with in real time.

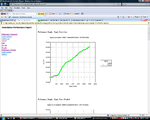

This setting as you can see goes back to 1993 and is profitable every year, so i have used one setting only to test this period, so therefore i have not optimised to suit so to speak, one setting for all trending and oscillation periods going back to 1993.

Results are not nothing great, but i feel also they cannot be random, to me there is a proven edge there, even if its only very tiny. Also the results do not take into account a better money management style and there is no compounding within the results you see there.

Anyway i have posted to get your opinions and also to debate that there is an adge to be found in using cycle analysis.

Results are based just on market, so anything that follows $indu works as ive tested this with similar, sometimes better performance.

this is far from my sole opinion, at the moment im very much into scalping using x trader after recently laerning somethings from a orderbook scalper, but i post for debate and also to argue cycle analysis can provide an edge, but its how we use the analysis that counts, for example trend following or meran reverting.

Pedro pete helped me program the following code about 18 months ago, since then ive had alot of stuff added to it which has improved performance.

No one seems to make money trading, not consistantly anyway, but i feel this is because you have to view it from another angle and not expect to win everyday and also ive found to smooth equity curve there is needs to be a few systems running or you make money from your job/business to counter act bad weeks, imo.

I have many many parameters, and below is not cherry picked and is far from the best performance report, i just posted a realistic tradeable report to get your opinions, this way im being true to myself and getting some real feedback.

I have gone through the code and tested for errors at every step possible in live real time, there is no bugs at present. I have added some realistic slippage to all trades, I have added comms. Execution is of course another matter and one i will feel with in real time.

This setting as you can see goes back to 1993 and is profitable every year, so i have used one setting only to test this period, so therefore i have not optimised to suit so to speak, one setting for all trending and oscillation periods going back to 1993.

Results are not nothing great, but i feel also they cannot be random, to me there is a proven edge there, even if its only very tiny. Also the results do not take into account a better money management style and there is no compounding within the results you see there.

Anyway i have posted to get your opinions and also to debate that there is an adge to be found in using cycle analysis.

Results are based just on market, so anything that follows $indu works as ive tested this with similar, sometimes better performance.

this is far from my sole opinion, at the moment im very much into scalping using x trader after recently laerning somethings from a orderbook scalper, but i post for debate and also to argue cycle analysis can provide an edge, but its how we use the analysis that counts, for example trend following or meran reverting.