HFM.

Senior member

- Messages

- 2,189

- Likes

- 0

Date: 2nd October 2023.

Market Update – October 2 – Shutdown postponed as Q4 kicks off.

Just a few hours before the Saturday midnight deadline, Democrats and Republicans passed a short term bill (45 days) to keep the government funded into November and avoid a shutdown which would have put the paychecks of some 3 million Americans in the public sector and the military at risk. This is certainly not an optimal and confidence-inducing solution in the long term: however, the markets are increasingly accustomed to such events, which have occurred over 20 times in the last 50 years, including 4 in the last decade. It may be this, it may be the start of the new quarter, it may be the good data from Asia, but this morning there is a slight risk on, with the US and European indices up by an average of +0.3% and oil also rising after two bad sessions that saw it pulling back from previous annual highs. The good news came from Asia, where manufacturing in China bounced back into the expansion zone for the first time since last April – as witnessed by the Caixin – and also in Japan, the Tankan Survey saw optimism grow in this side of the productive tissue. This morning we are also seeing very different calls from 2 major US investment banks, with GS seeing demand for both oil and copper booming in China while CITI is taking the opposite view and sees weakness in industrial metals – with possible falls in the range of 5-10% – and Crude falling to $70 in early 2024. However, after September proved to be a particularly negative month with falls of up to 5.8% in the case of the Nasdaq, investors want to start off on the right foot and celebrate the agreement reached in Washington at the same time as they anticipate Federal Reserve Chairman Jerome Powell’s remarks later today.

UKOil – USOil spread is narrowing

Interesting Mover: XAGUSD (-1.44% @ $21.88) had a wild session on Friday with a sharp reversal and an excursion of 6.16%. The trendline that originated in August 2022 has been broken, but there is another longer-term one currently passing through the $20.50 area, while $21.50 is a strong static support; the price is below its 50d and 200d MAs.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 2 – Shutdown postponed as Q4 kicks off.

Just a few hours before the Saturday midnight deadline, Democrats and Republicans passed a short term bill (45 days) to keep the government funded into November and avoid a shutdown which would have put the paychecks of some 3 million Americans in the public sector and the military at risk. This is certainly not an optimal and confidence-inducing solution in the long term: however, the markets are increasingly accustomed to such events, which have occurred over 20 times in the last 50 years, including 4 in the last decade. It may be this, it may be the start of the new quarter, it may be the good data from Asia, but this morning there is a slight risk on, with the US and European indices up by an average of +0.3% and oil also rising after two bad sessions that saw it pulling back from previous annual highs. The good news came from Asia, where manufacturing in China bounced back into the expansion zone for the first time since last April – as witnessed by the Caixin – and also in Japan, the Tankan Survey saw optimism grow in this side of the productive tissue. This morning we are also seeing very different calls from 2 major US investment banks, with GS seeing demand for both oil and copper booming in China while CITI is taking the opposite view and sees weakness in industrial metals – with possible falls in the range of 5-10% – and Crude falling to $70 in early 2024. However, after September proved to be a particularly negative month with falls of up to 5.8% in the case of the Nasdaq, investors want to start off on the right foot and celebrate the agreement reached in Washington at the same time as they anticipate Federal Reserve Chairman Jerome Powell’s remarks later today.

UKOil – USOil spread is narrowing

- FX – USDIndex just shy of 106, +0.15% @ 105.97; AUDUSD is the laggard among majors -0.30% @ 0.6414, USDJPY is trading at 149.65 after having hit a new 2023 high at 149.82. EURUSD flat, GBPUSD @ 1.22.

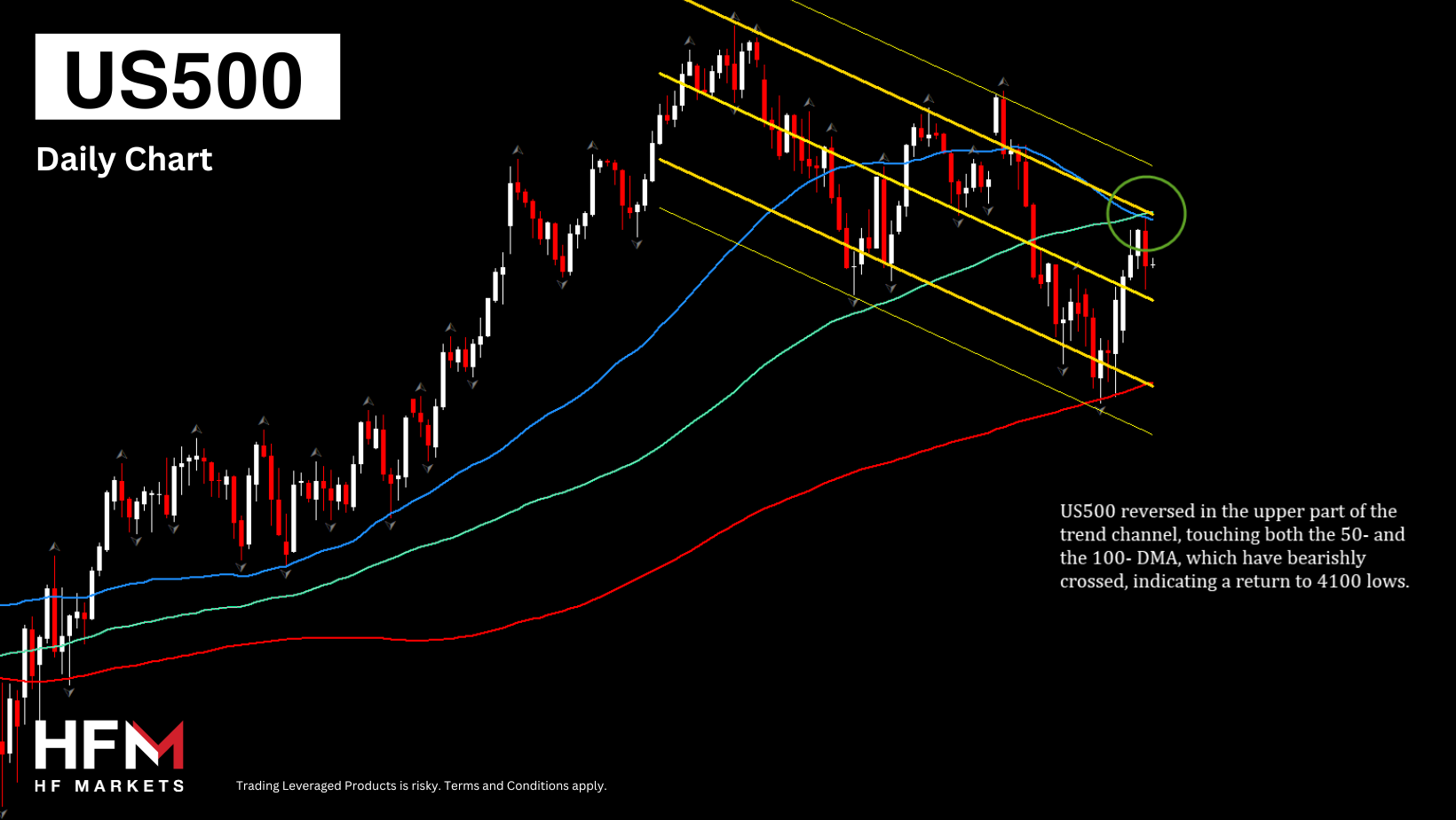

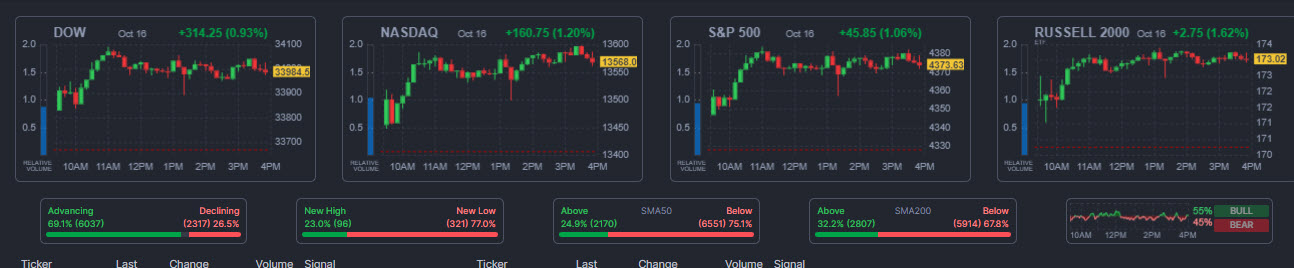

- Stocks – US Futures are inching higher (US500 +0.40%, US100 +0.50%, US30 +0.39%%); EU futures are up as well (GER40 +0.35%, FRA40 +0.41%). September was a grim month: US30 -3.5%, US500 –4.9%, US100 -5.8%. Performances were negative for the whole Q3: -2.6%, -3.7%, -4.1% respectively.

- Commodities – USOil +0.64% at $91.32, UKOil is trading at $92.65 and their spread has narrowed to just $1.33, in the lower bound of this year’s range.

- GOLD – -0.19% @ $1845, XAGUSD adds another -1.44% to its recent prolonged drop, trading at $21.88.

Interesting Mover: XAGUSD (-1.44% @ $21.88) had a wild session on Friday with a sharp reversal and an excursion of 6.16%. The trendline that originated in August 2022 has been broken, but there is another longer-term one currently passing through the $20.50 area, while $21.50 is a strong static support; the price is below its 50d and 200d MAs.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.