HFM.

Senior member

- Messages

- 2,064

- Likes

- 0

Date: 10th July 2024.

Market News – Stocks advance, Kiwi & Dollar dip.

Economic Indicators & Central Banks:

The rising political uncertainties, and the wait for more data to clarify the Fed’s rate cut path, are combining with summer doldrums to keep trading quiet and range bound.

Asian & European Open:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks advance, Kiwi & Dollar dip.

Economic Indicators & Central Banks:

The rising political uncertainties, and the wait for more data to clarify the Fed’s rate cut path, are combining with summer doldrums to keep trading quiet and range bound.

- Fed Chair Powell did not say anything really new in his Senate testimony, as expected. There were a few nuances, though, that further support expectations that the next move will be a cut.

- Financials led the way for the broad index after Chair Powell indicated a re-proposal for Basel III rules would be sent out, giving banks more time and breathing room.

- RBNZ delivers dovish hold, as the comments set the stage for a rate cut later in the year and the NZD weakened as local bonds rallied. New Zealand’s central bank maintained its official cash rate at 5.50%, but signalled that it is inching closer to a rate cut. The statement said “restrictive monetary policy has significantly reduced consumer price inflation, with the committee expecting headline inflation to return to within the 1-3 percent target range in the second half of the year.”

- China’s consumer prices saw a slight increase in June, staying close to zero for the 5th month, indicating ongoing deflationary pressures hindering economic recovery. Meanwhile, factory-gate prices remained in deflation.

- Japan’s largest banks urged the Bank of Japan to significantly reduce its monthly bond purchases during recent central bank hearings.

Asian & European Open:

- Wall Street and Treasuries were mixed. The S&P500 advanced 0.10% to 5577, a 6th straight day of gains (the best since the start of the year) and another fresh high, the 36th record for 2024. The NASDAQ was 0.11% firmer at 18,429, also at a new peak, its 26th for the year.

- Japanese stocks advanced, while those in China and Australia declined. Nikkei surged to another record high, approaching 42,000.

- The heavy tilt towards the tech sector has heightened risks if the AI-driven rally stumbles. Valuations are high, and earnings growth is expected to slow, adding uncertainty for investors banking on Big Tech’s continued rise. Citigroup strategists, suggest it might be time to take profits in leading AI stocks, despite strong sentiment and better-than-expected free cash flow projections for these firms.

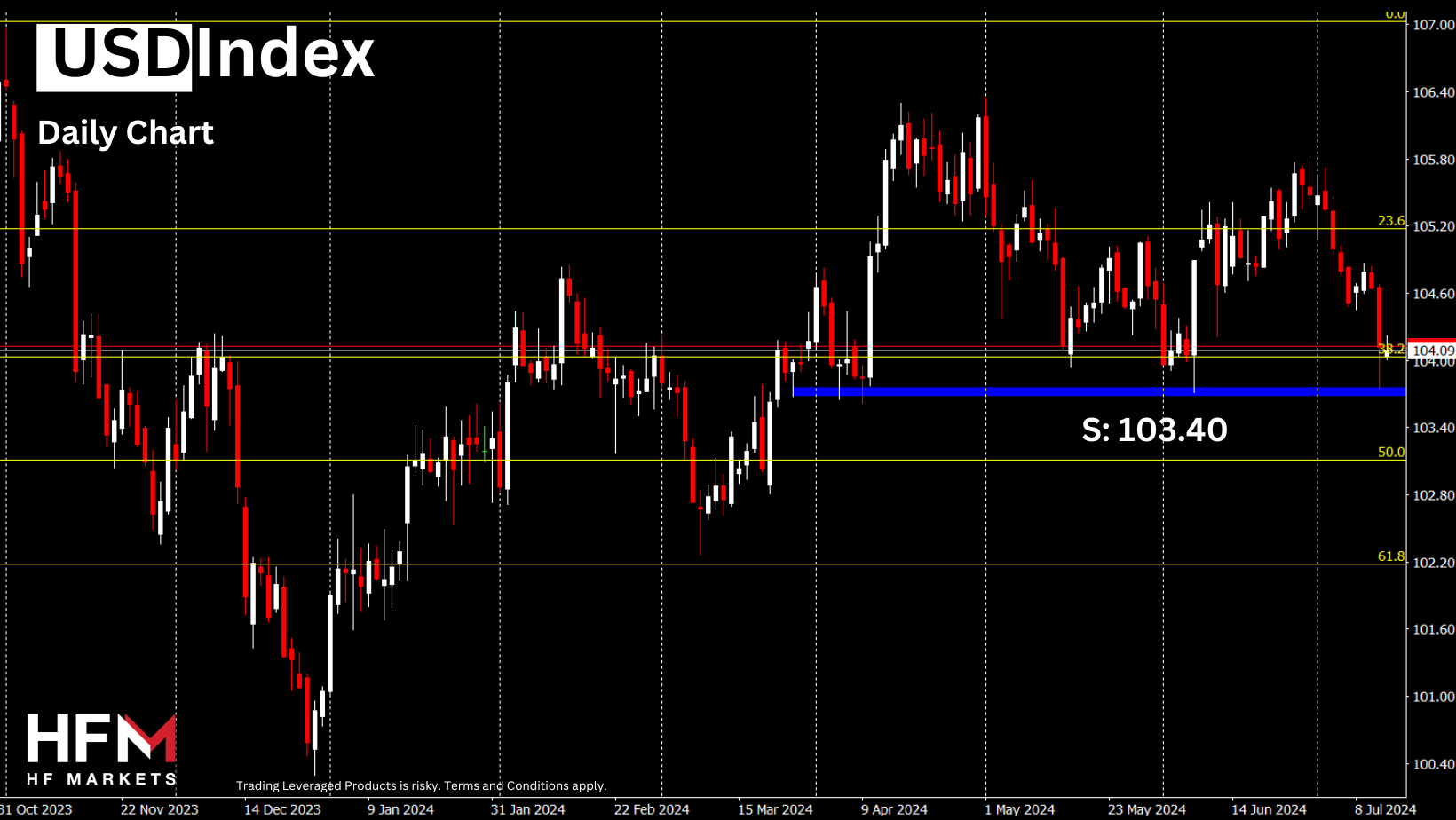

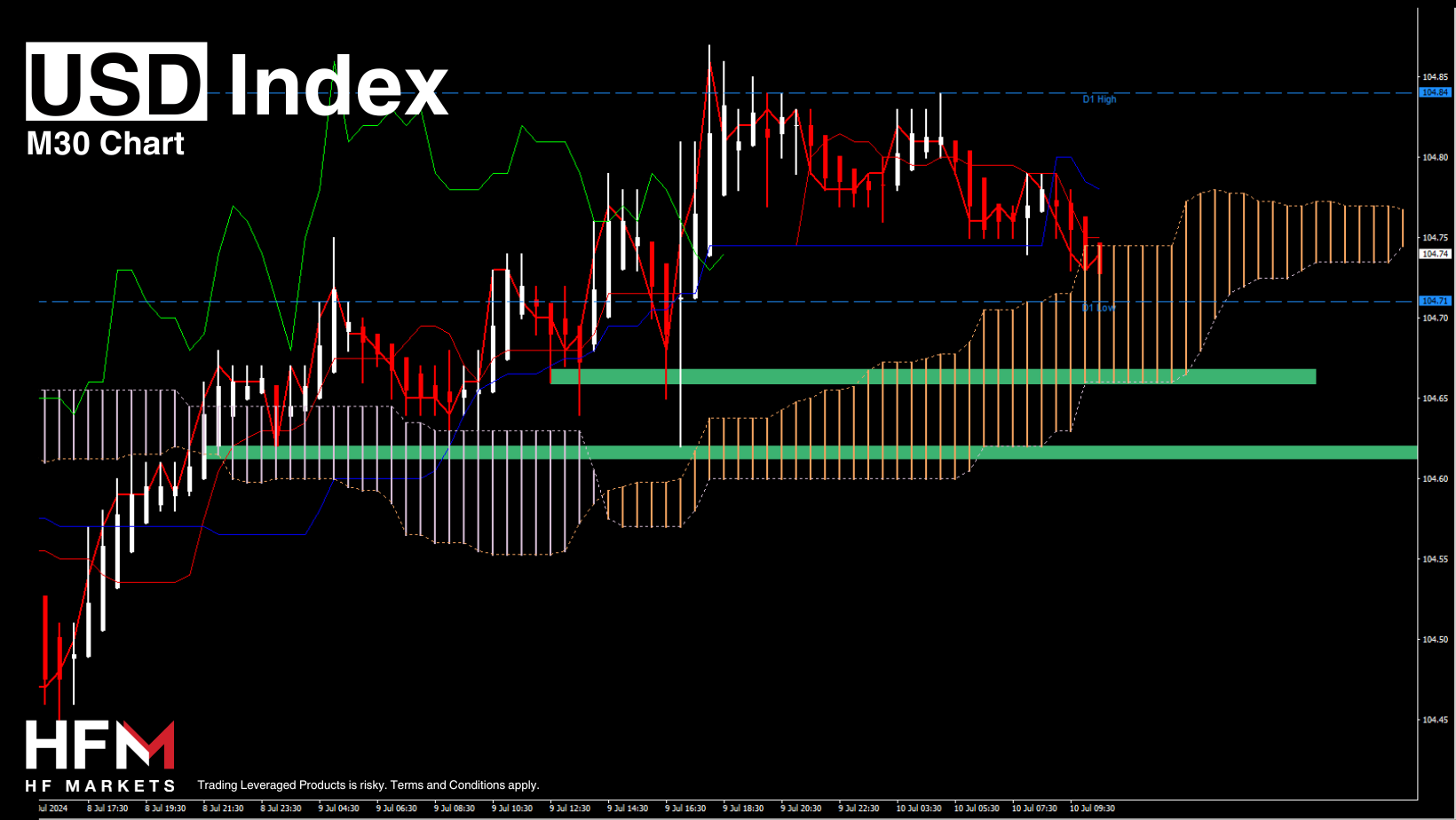

- The USDIndex declined from 105.208 back to 104.70.

- Oil prices have continued to decline, as Chinese demand and continued uncertainty over the timeline for Fed interest rate cuts outweighed signs of another inventory draw in the US.

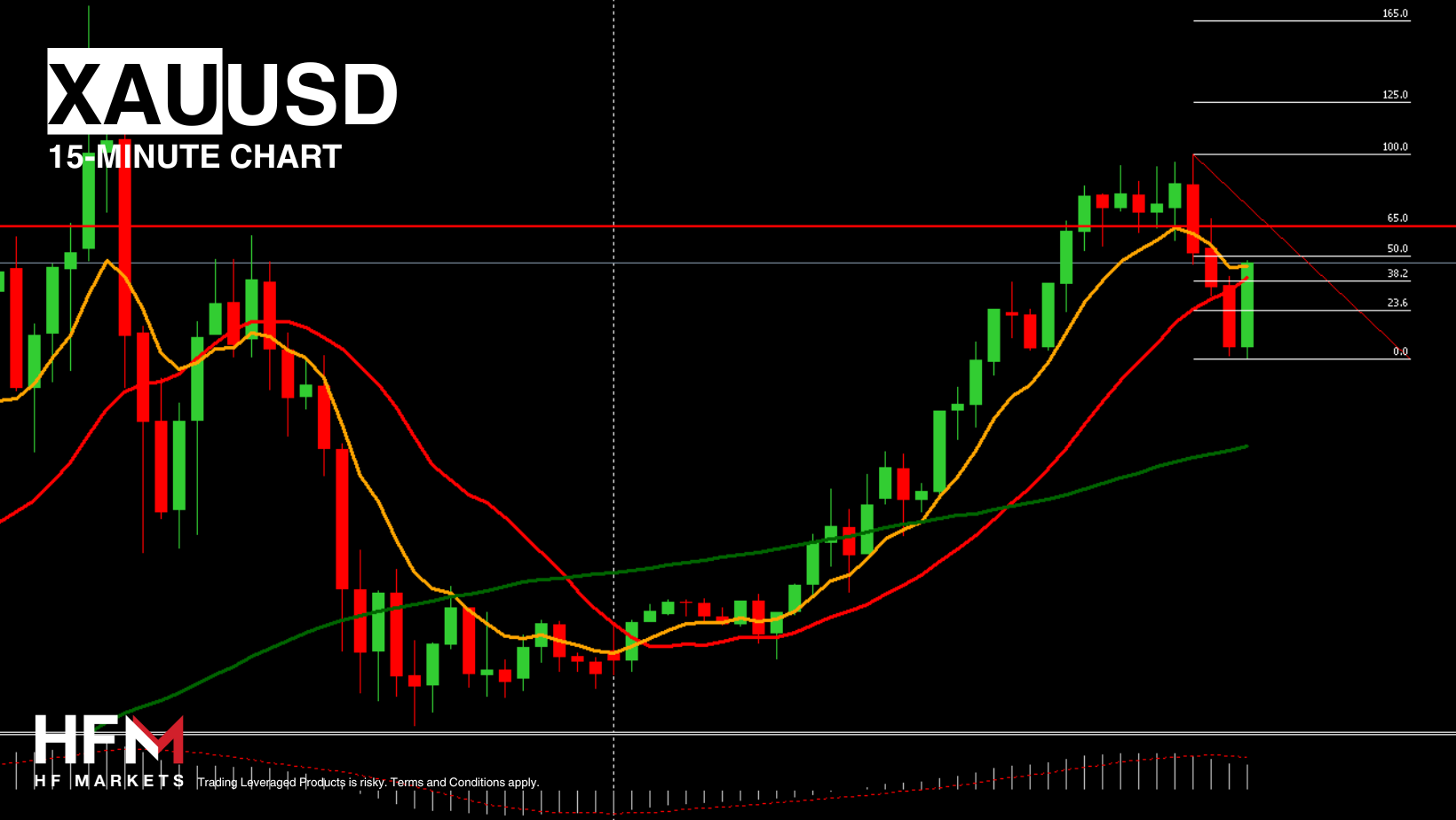

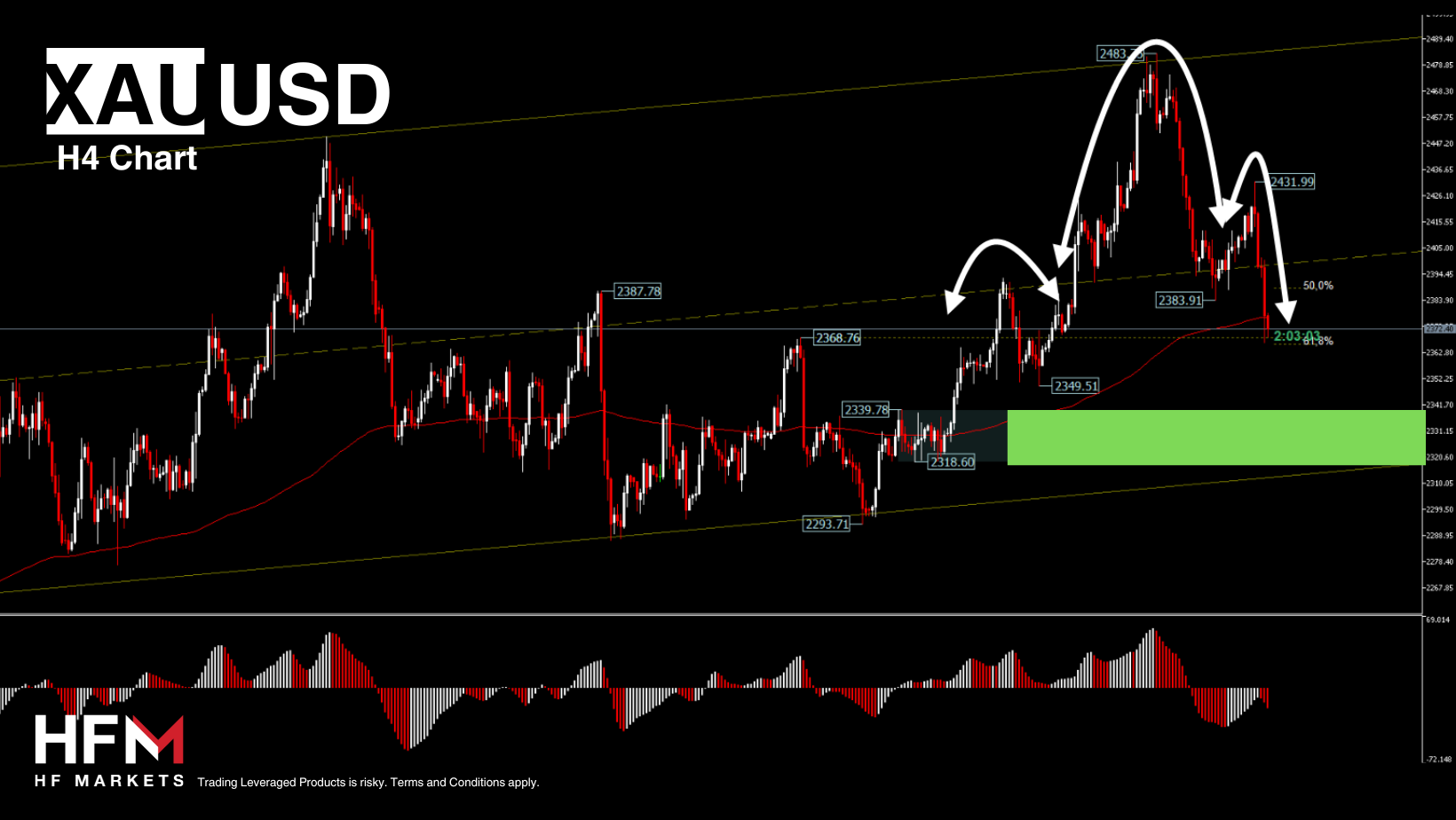

- Gold slightly higher at 2372 amid Dollar strength.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.