Looking for feedback on the following.

This is a breakout system i have made and was wondering what people thought in terms of what should be improved.

Win ratio very low, but im looking to run it mechanically on the markets.

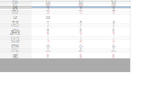

Tested on YM from 1998 - 2010 feedback appreciated.

Also attached (dodgy looking equity curve and yearly breakdown).

Anything i should watch out for?

This is a breakout system i have made and was wondering what people thought in terms of what should be improved.

Win ratio very low, but im looking to run it mechanically on the markets.

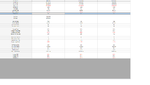

Tested on YM from 1998 - 2010 feedback appreciated.

Also attached (dodgy looking equity curve and yearly breakdown).

Anything i should watch out for?